Assessing the 2021 Ontario Budget

1 | Key Points

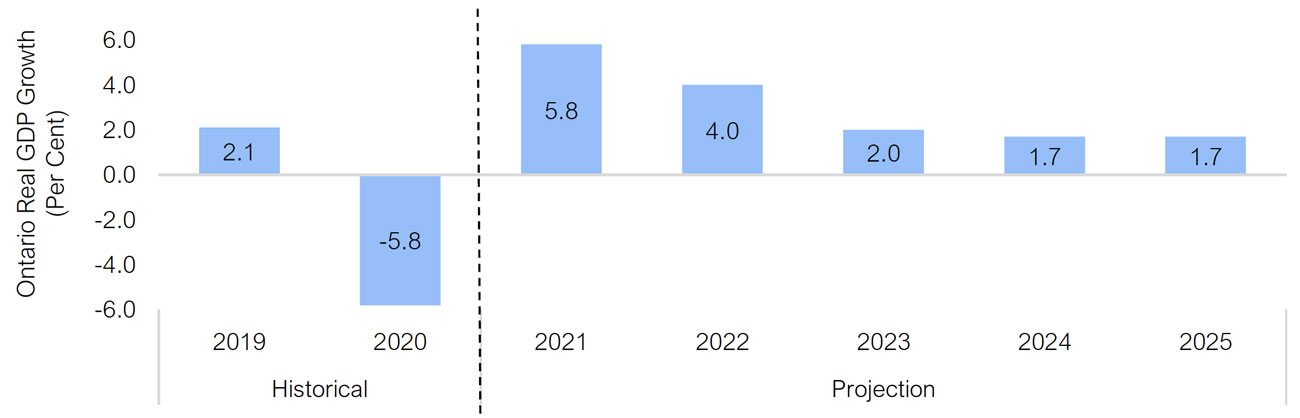

- Ontario’s economy is expected to rebound strongly over the next two years, fueled by continued COVID-19 vaccinations, improving global demand and ongoing monetary and fiscal policy support. The FAO projects Ontario real GDP will rise by 5.8 per cent in 2021 and 4.0 per cent in 2022.

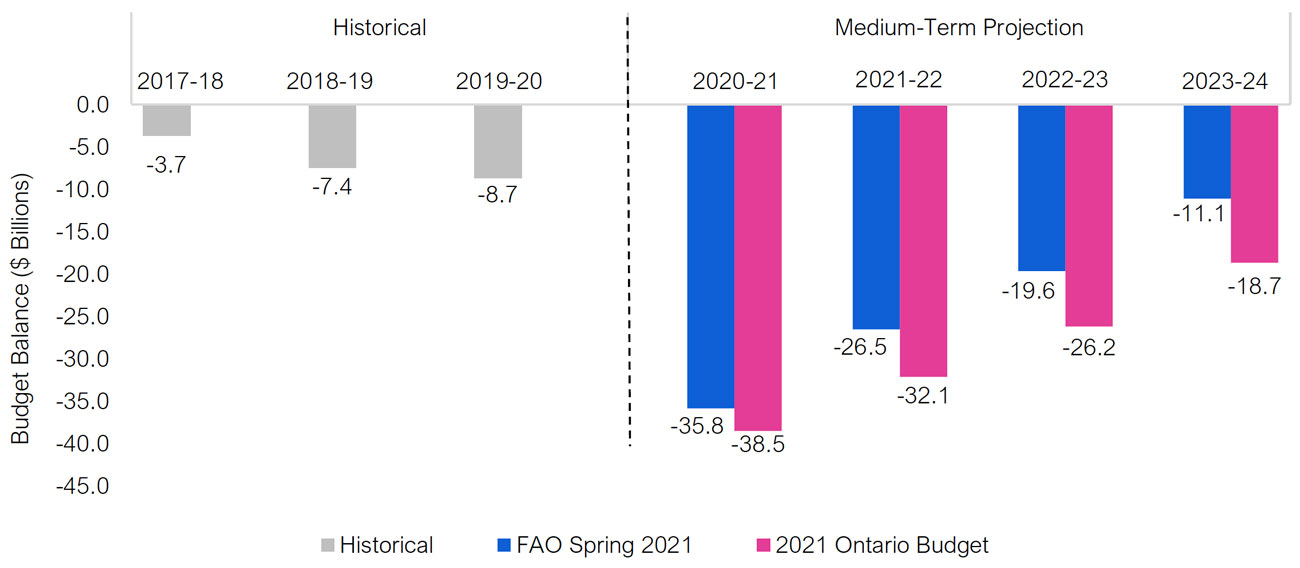

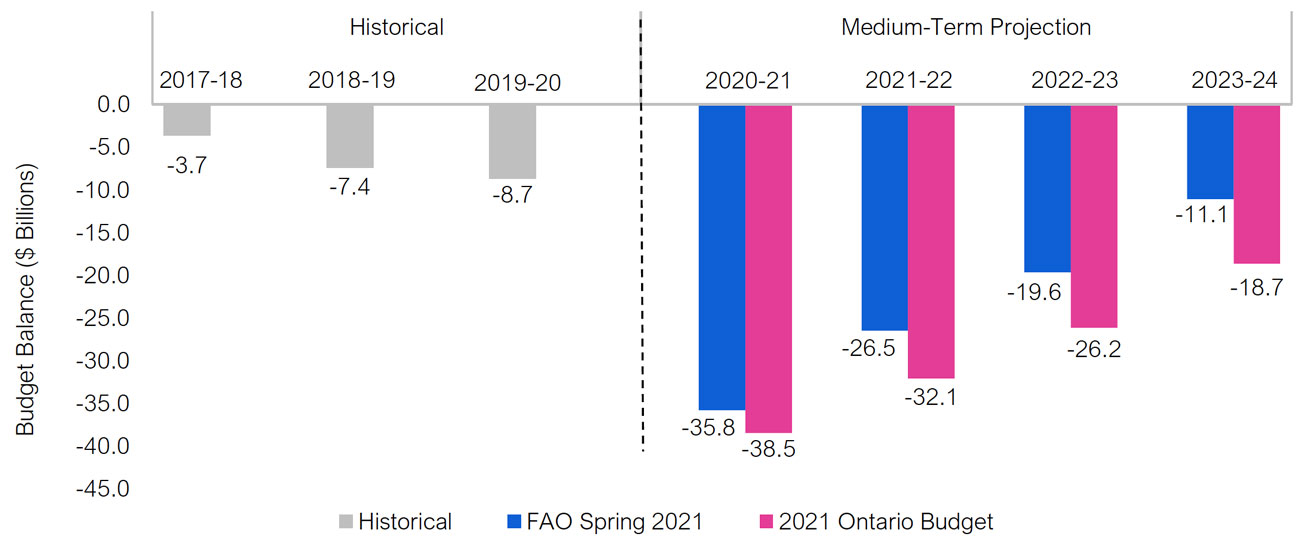

- The COVID-19 pandemic caused a decline in revenue and a significant increase in program spending, leading to a record budget deficit of $35.8 billion in 2020–21. As the economy rebounds, rising revenues are expected to help lower the budget deficit to $11.1 billion in 2023–24. In contrast, the government projects an $18.7 billion deficit in 2023–24 mainly due to its significantly weaker revenue outlook.

- The budget’s revenue forecast is lower than what the government’s economic outlook would suggest. The FAO estimates that the budget’s revenue projection would be higher by about $1.4 billion in 2022–23 and $2.2 billion in 2023–24, based on the usual relationships between tax revenue and economic growth. Although not announced in the 2021 budget, these revenue shortfalls might be explained by potential planned tax cuts.

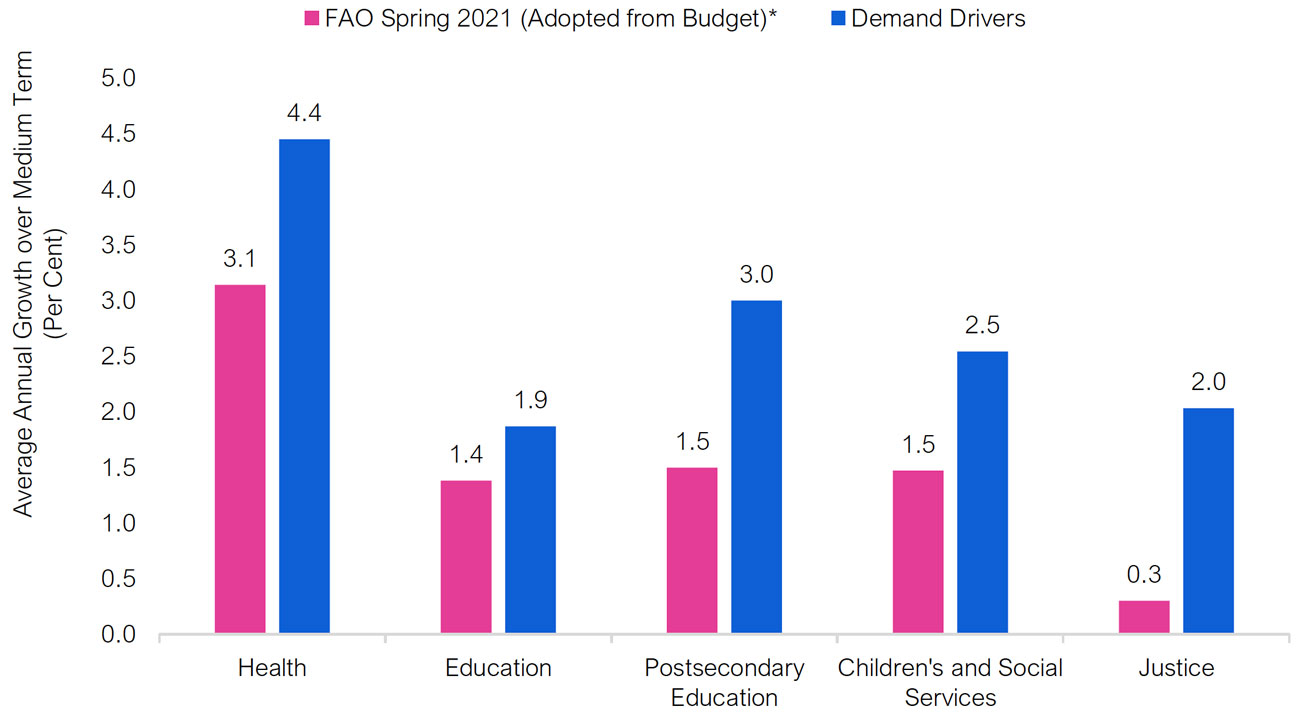

- Excluding temporary COVID-19 funds, planned program spending growth increases sharply in 2021–22 and slows significantly afterwards. The FAO finds the budget’s planned program spending growth in key sectors, including health and education, will not keep pace with the underlying demand for public services over the medium-term projection.

- In the 2021 Ontario budget, the government presented a recovery plan that projected a path to a balanced budget by 2029–30. However, the government’s recovery plan relies on prolonged spending restraint that would require $17.8 billion in permanent cost savings. The budget provided no details on how this would be achieved.

- The government is not expected to achieve a balanced budget by 2029–30 under current policies. The FAO’s projection shows a deficit of $6.9 billion in 2029–30, which is $9.3 billion below the government’s projected $2.4 billion surplus.

- Even with ongoing budget deficits over the recovery plan, the FAO expects Ontario’s fiscal indicators, including the province’s net debt-to-GDP ratio and interest on debt as a share of revenue, to improve over the projection. However, if interest rates rise above the expected growth in the economy, these indicators could be adversely impacted.

2 | Summary

Ontario economy expected to grow strongly in 2021

Following the severe decline in economic activity at the onset of the COVID-19 pandemic, Ontario’s economic growth has been generally resilient despite recurring restrictions. Improving global demand, ongoing monetary and fiscal policy support, and progress in COVID-19 vaccinations have set the stage for a strong economic rebound in Ontario over the next two years.

Figure 2‑1: Ontario economy expected to rebound strongly in 2021 and 2022

Source: Ontario Economic Accounts and FAO.

Assuming Ontario’s vaccine distribution proceeds as planned[1] and the pandemic subsides, the FAO projects Ontario real GDP will rise by 5.8 per cent in 2021. As the majority of the Canadian population becomes immunized and the economy is fully reopened, strong economic growth is expected to continue in 2022, with real GDP rising by 4.0 per cent. However, if the vaccination plan is disrupted or the government’s public health measures are unable to contain new COVID-19 variants, economic growth would be slower.

Revenues rebound in 2021–22

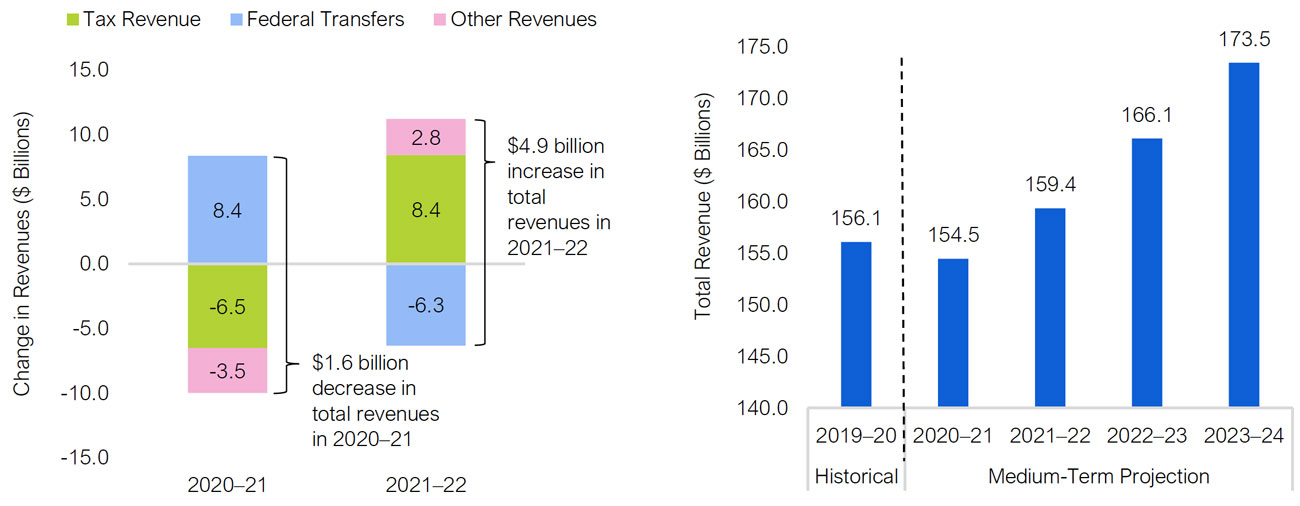

Total revenue is expected to decline modestly by $1.6 billion in 2020–21 from 2019–20, despite the substantial drop in economic activity caused by the COVID-19 pandemic. Sharp declines in tax and ‘Other’ revenues in 2020–21, are largely offset by a significant $8.4 billion increase in transfers from the federal government—primarily consisting of one-time COVID-related support. In 2021–22, total revenue is expected to rebound by $4.9 billion as COVID-19 vaccinations become more widely available and the recovery in economic activity strengthens. Over the remainder of the medium-term outlook (2022–23 to 2023–24) total revenue is expected to grow at an average annual rate of 4.3 per cent, consistent with the FAO’s outlook for economic growth. By 202324, the FAO’s revenue outlook is $6.5 billion higher than the budget’s projection.

In addition, the 2021 Ontario budget’s revenue forecast is lower than what the government’s own economic outlook would suggest. The FAO estimates that the budget’s revenue projection would be higher by about $1.4 billion in 2022–23 and $2.2 billion in 2023–24, based on the usual relationships between tax revenue and economic growth. Although not announced in the 2021 budget, these revenue shortfalls might suggest planned tax cuts.

Base program spending growth slows after 2021–22

Base program spending growth (excluding pandemic-related temporary expenses) increases sharply by 5.4 per cent in 2021–22 and slows significantly afterwards. In particular, the government plans to grow base program spending by just 0.8 per cent in 2023–24. Compared to the 2021 Ontario budget, planned program spending growth in key sectors will not keep pace with underlying demand for public services over the medium term.

Figure 2‑2: Base program expense growth in key sectors will not keep pace with demand drivers

*FAO Spring 2021 program spending projection is adopted from the 2021 Ontario Budget.

Note: The average annual growth rates over the medium term in different sectors refer to base program spending and do not include any COVID-19 related spending.

Source: 2021 Ontario Budget and FAO.

FAO projects smaller deficits over the medium term compared to the government

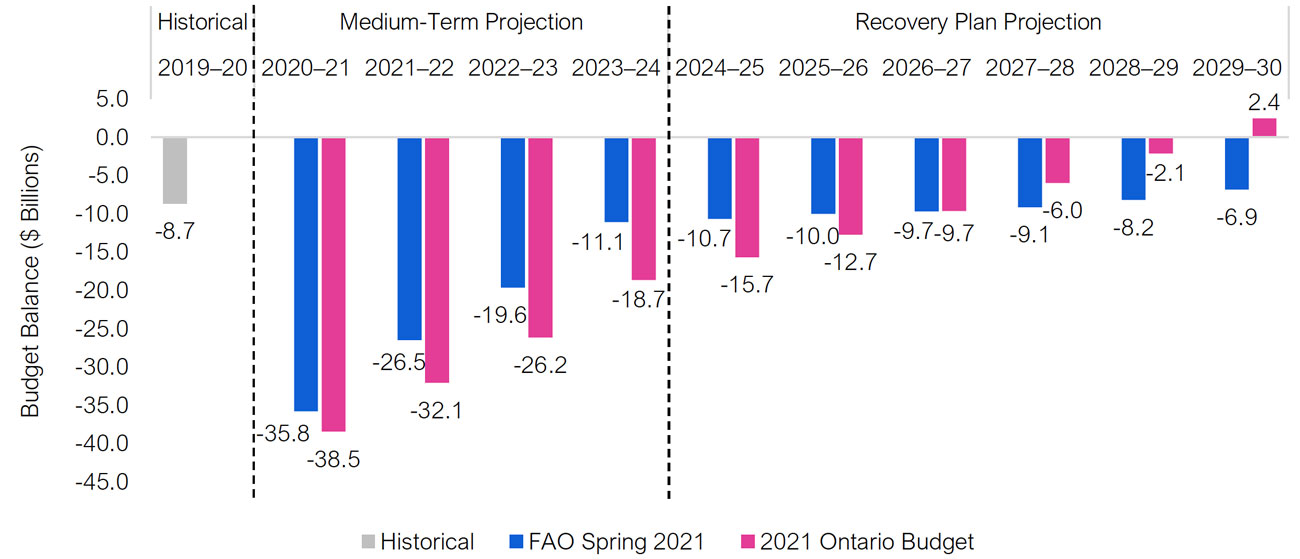

After posting a record budget deficit of $35.8 billion in 2020–21, the FAO expects that Ontario’s deficits will improve over the medium term as the province recovers from the COVID-19 pandemic and the economy rebounds. The FAO projects that under current policies, Ontario’s deficit would decline from $26.5 billion in 2021–22 to $11.1 billion by 2023–24, a significant improvement but still larger than the $8.7 billion deficit recorded before the pandemic in 2019–20.

In contrast, the government’s deficit forecast improves substantially slower than the FAO’s projection. By 2023–24, the FAO expects the deficit to be $7.6 billon smaller than the government’s deficit projection of $18.7 billion. This difference results from the FAO’s higher revenue projection combined with a lower interest on debt forecast.

Figure 2‑3: Ontario’s budget deficits projected to be smaller compared to the government’s plan

The Budget Balance is presented without the reserve.

Source: 2021 Ontario Budget and FAO.

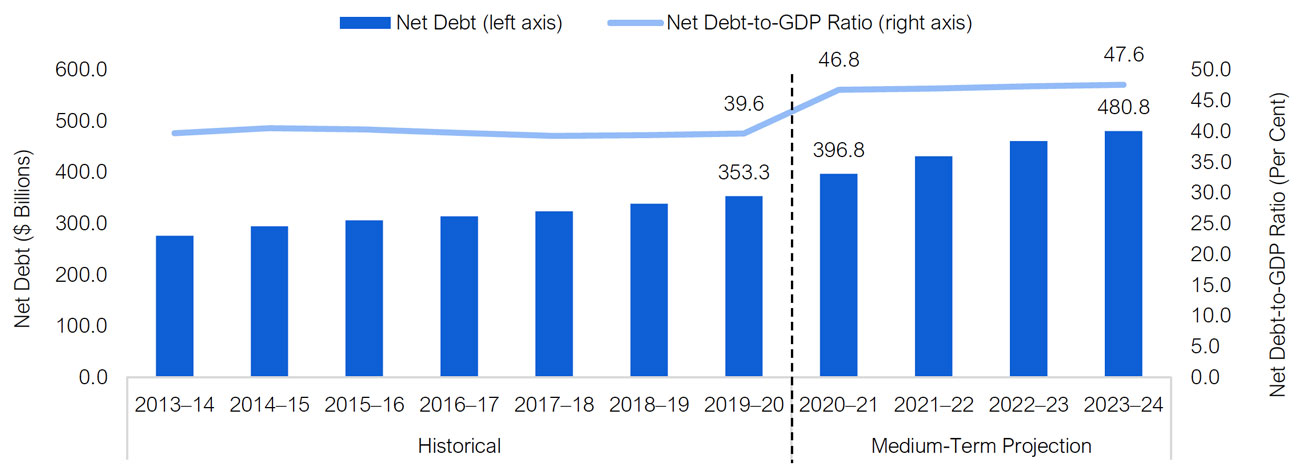

Net debt is expected to rise sharply in 2020–21, increasing by $43.5 billion to $396.8 billion. The substantial increase in net debt results in a large jump in the net debt-to-GDP ratio, which reaches 46.8 per cent in 2020–21. Even with stronger economic growth and declining deficits, the net debt-to-GDP ratio rises to 47.6 per cent in 2023–24, which is eight percentage points higher than the pre-pandemic ratio of 39.6 per cent in 2019–20.

The province is not expected to balance the budget by 2029–30

According to Ontario’s Fiscal Sustainability, Transparency and Accountability Act 2019 (FSTAA), the government is required to present a recovery plan to balance the budget if there is a deficit by the end of the current multi-year plan. In the 2021 Ontario budget, the government presented a recovery plan that projected a path to a balanced budget by 2029–30. However, the government’s recovery plan relies on prolonged spending restraint that would require significant and permanent cost savings that have historically been difficult to achieve.

To assess the government’s plan, the FAO developed an independent fiscal projection over the recovery period, incorporating a revenue and program spending outlook based on economic and demographic drivers. In the FAO’s projection, Ontario is not expected to achieve a balanced budget by 2029–30. The FAO forecasts a deficit of $6.9 billion under current policies, $9.3 billion below the government’s projected $2.4 billion surplus.

Figure 2‑4: Ontario’s budget will not be balanced by 2029-30

Note: Budget Balance is presented before the reserve.

Source: 2021 Ontario Budget and FAO.

Despite the large ongoing deficits, Ontario’s fiscal indicators are expected to improve over the projection following sharp deteriorations in 2020–21 caused by the pandemic. The province’s net debt-to-GDP ratio is expected to decline modestly to 44.7 per cent by 2029–30, just below the 46.8 per cent in 2020–21. Similarly, debt interest payments as a share of revenue decline from 8.1 per cent in 2020–21 to 7.3 per cent by 2029–30, the lowest since 1982–83.

The improvement in Ontario’s fiscal metrics is driven by the FAO’s projection that economic growth will exceed the province’s effective borrowing rate. However, if interest rates rise higher than the rate of economic growth, Ontario’s debt indicators would begin to deteriorate, increasing interest on debt payments relative to revenues and potentially pushing the province’s debt burden above the government’s targeted limit of 50.5 per cent.

3 | Economic Outlook

Overview

Despite the COVID-19 pandemic and the recent re-enaction of public health restrictions, Ontario’s economic growth has been generally resilient in late 2020 and early 2021, with sales activity rising and the job market continuing to recover. Improving global demand, ongoing monetary and fiscal policy support, and progress in COVID-19 vaccinations have set the stage for a strong economic rebound in Ontario over the next two years.

Assuming Ontario’s vaccine distribution proceeds as planned[2] and the pandemic subsides, the FAO projects Ontario real GDP will rise by 5.8 per cent in 2021. As the majority of the Canadian population becomes immunized and the economy is fully reopened, strong economic growth is expected to continue in 2022, with real GDP rising by 4.0 per cent. However, if the vaccination plan is disrupted or the government’s public health measures are unable to contain new COVID-19 variants, economic growth would be slower this year.

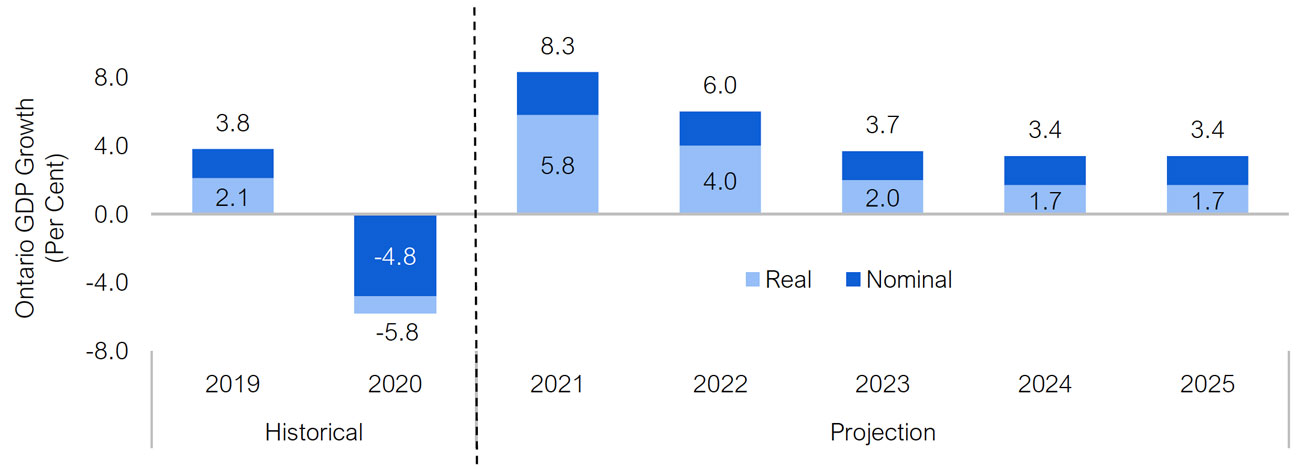

Ontario nominal GDP, which provides a broad measure of the tax base, is projected to rise by 8.3 per cent in 2021 and 6.0 per cent in 2022, reflecting a strong recovery in labour income and corporate profits.

Figure 3‑1: Ontario economy expected to rebound strongly in 2021 and 2022

Source: Ontario Economic Accounts and FAO.

Global economy projected to grow strongly in 2021

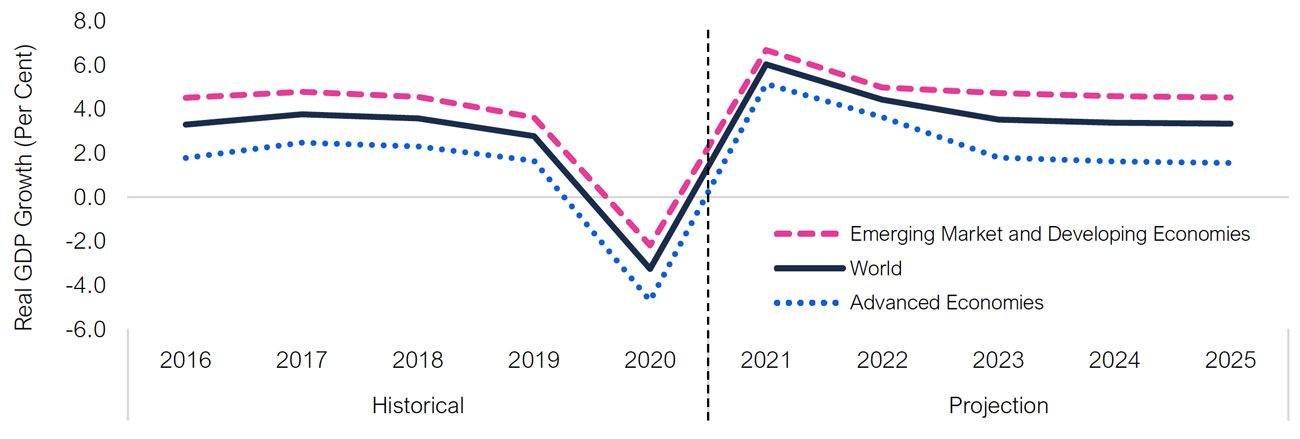

Following the severe decline in global economic activity in 2020, significant government spending, historically low interest rates and the increasing availability of COVID-19 vaccines will provide support for a strong global recovery in 2021. Although new COVID-19 infection waves and variants have led to renewed shutdown measures in many countries, global economic growth is generally improving. Based on these developments, the International Monetary Fund (IMF) projects the global economy will rise by 6.0 per cent in 2021, a considerable upward revision from their assessment earlier this year.[3] The rate of economic recovery is expected to remain uneven across countries due to differences in the pace of vaccine rollout, the extent of policy support and industrial composition.

Figure 3‑2: Global real GDP projected to rise by 6.0 per cent in 2021

Source: International Monetary Fund.

In the United States, the rapid distribution of COVID-19 vaccines and the US$1.9 trillion fiscal stimulus in March have erased concerns of a slow recovery. U.S. real GDP is now projected to rise by 6.4 per cent in 2021, the fastest pace among advanced economies.[4] In recent months, gains in employment, consumer spending and business activity have surpassed expectations, pointing to a strong start to economic growth this year. Even though inflation is running above the two per cent target, the Federal Reserve is expected to keep interest rates low until its long-run goals for employment and inflation are met.[5]

In Canada, the projection for real GDP growth in 2021 has improved to 5.9 per cent, strengthened by expanded vaccine availability, rising commodity prices, and a brighter outlook for exports from stronger growth in the United States. Ongoing federal support for households and businesses, notably the Canada Recovery Benefit, Canada Emergency Wage Subsidy and Canada Emergency Business Account, will continue to help individuals and businesses manage the financial strain of the COVID-19 pandemic.[6] Strong employment gains are expected as the economy is fully reopened over the course of the year, especially in service sectors that have faced prolonged government restrictions. Heightened activity in the housing market, driven by record-low borrowing rates, is expected to persist as households increasingly prefer ownership over rental arrangements.[7]

Interest rates to remain low until 2022

Source: Statistics Canada and FAO.

Source: Statistics Canada and FAO.

The Bank of Canada has maintained its policy interest rate[8] at 0.25 per cent since March 2020, when the rate was lowered by 1.5 percentage points in response to the economic downturn. In recent months, the Bank announced its intention to phase out some emergency measures such as the provincial bond buying program,[9] but is expected to hold its policy interest rate at 0.25 per cent until the annual inflation target of two per cent is sustainably achieved.[10] Based on the recent rise in long-term bond yields and the upward revisions to the Bank’s outlook for the Canadian economy and inflation, interest rates are expected to rise sooner than previously projected, possibly beginning in the second half of 2022.

Ontario economy expected to rebound strongly in 2021 and 2022

Although the government re-enacted public health restrictions in response to the second and third waves of infections and hospitalizations in late 2020 and early 2021, economic activity has been generally resilient as many households and businesses adapted. COVID-19 vaccine distribution in Ontario has become available for many age groups, setting the stage for the economy to reopen more fully. With improving global demand and ongoing monetary and fiscal policy support, Ontario is expected to record strong economic growth over the next two years.

Assuming current plans for the vaccine rollout proceed as scheduled, the FAO projects Ontario real GDP will rise by 5.8 per cent in 2021. As much of the population becomes immunized and the economy is fully reopened, economic growth is expected to remain strong in 2022, with real GDP rising by 4.0 per cent. However, if the vaccination plan is disrupted or the government’s public health measures are unable to contain new COVID-19 variants, economic growth would be slower this year.

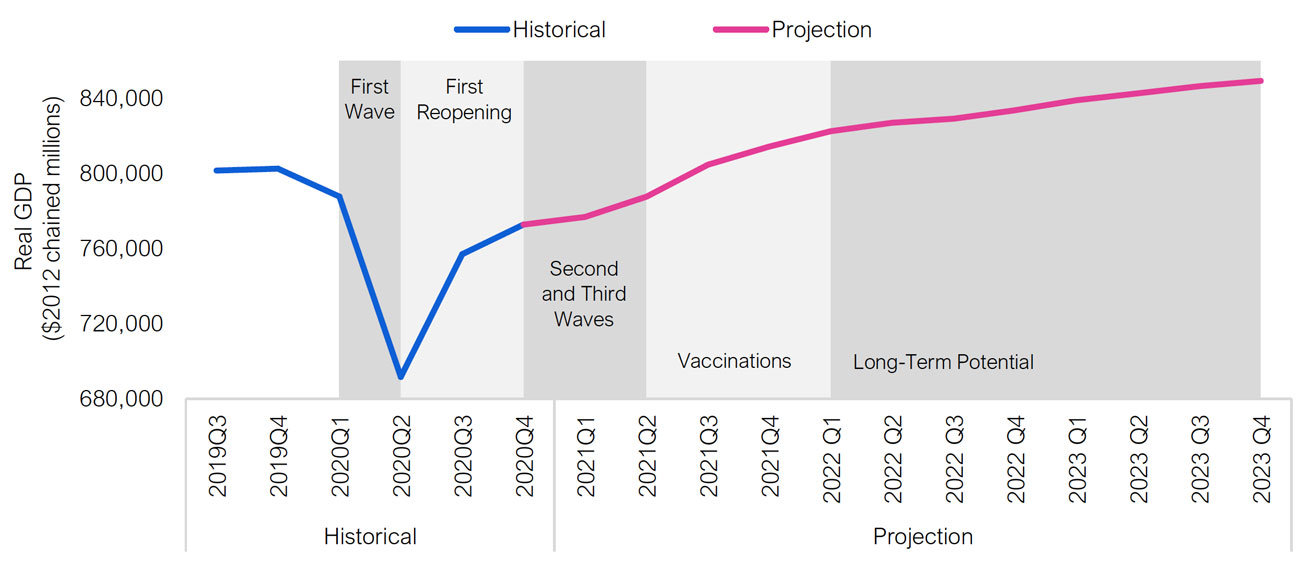

Over the 2023 to 2025 period, Ontario’s economy is expected to return to long-term trends, with average annual real GDP growth of 1.8 per cent.

Figure 3‑4: Ontario real GDP growth to improve

Source: Ontario Economic Accounts and FAO.

Strong recovery is projected broadly across the economy. Consumer spending should accelerate throughout the year, supported by pent-up demand and elevated household savings. Residential investment, fueled by record low mortgage rates and heightened activity in the housing market, is projected to increase rapidly over the next two years. Exports will benefit from strong consumer demand and manufacturing activity in the United States. Business investment is expected to recover as firms become confident economic growth will persist and a stronger Canadian dollar lowers the cost of imported machinery and equipment.

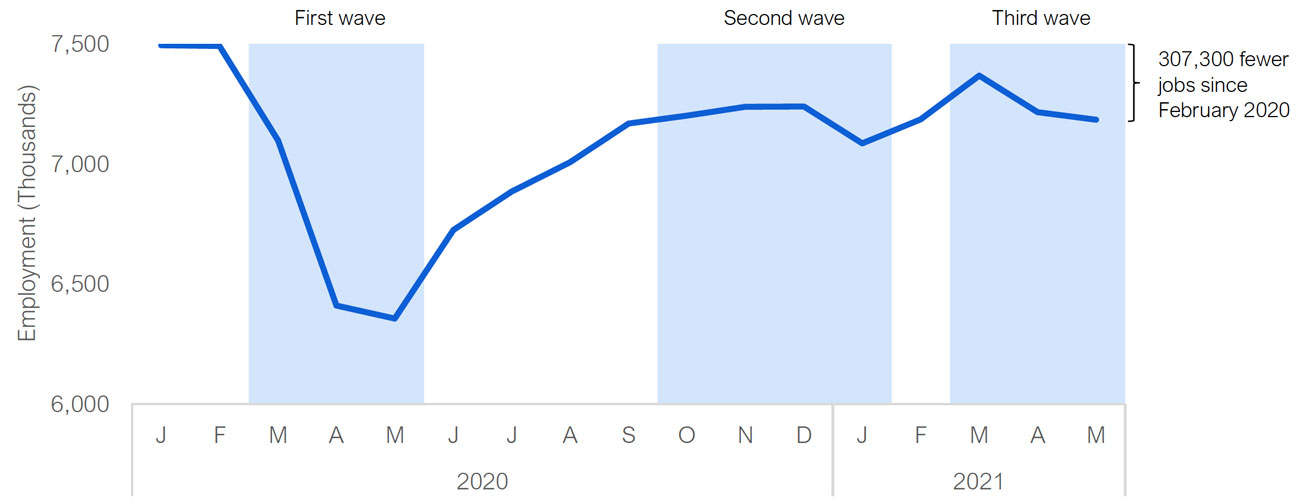

After record job losses in the spring of 2020 during the first wave of the pandemic, employment has increased, although the pace has been uneven due to shifting public health restrictions. As of May 2021, employment remains down by 307,300 jobs (or -4.1 per cent) compared to the pre-pandemic level in February 2020.

Figure 3‑5: Ontario’s employment still 275,700 jobs below pre-pandemic levels

Source: Statistics Canada and FAO.

As the economy improves over the next two years, job growth will continue to rebound, and the annual level of employment is projected to surpass its pre-pandemic peak in 2022. The unemployment rate is projected to gradually trend down to pre-pandemic levels towards the end of the outlook.

Figure 3‑6: Unemployment rate to trend down to pre-pandemic levels

Source: Statistics Canada and FAO.

Source: Ontario Economic Accounts and FAO.

Source: Ontario Economic Accounts and FAO.

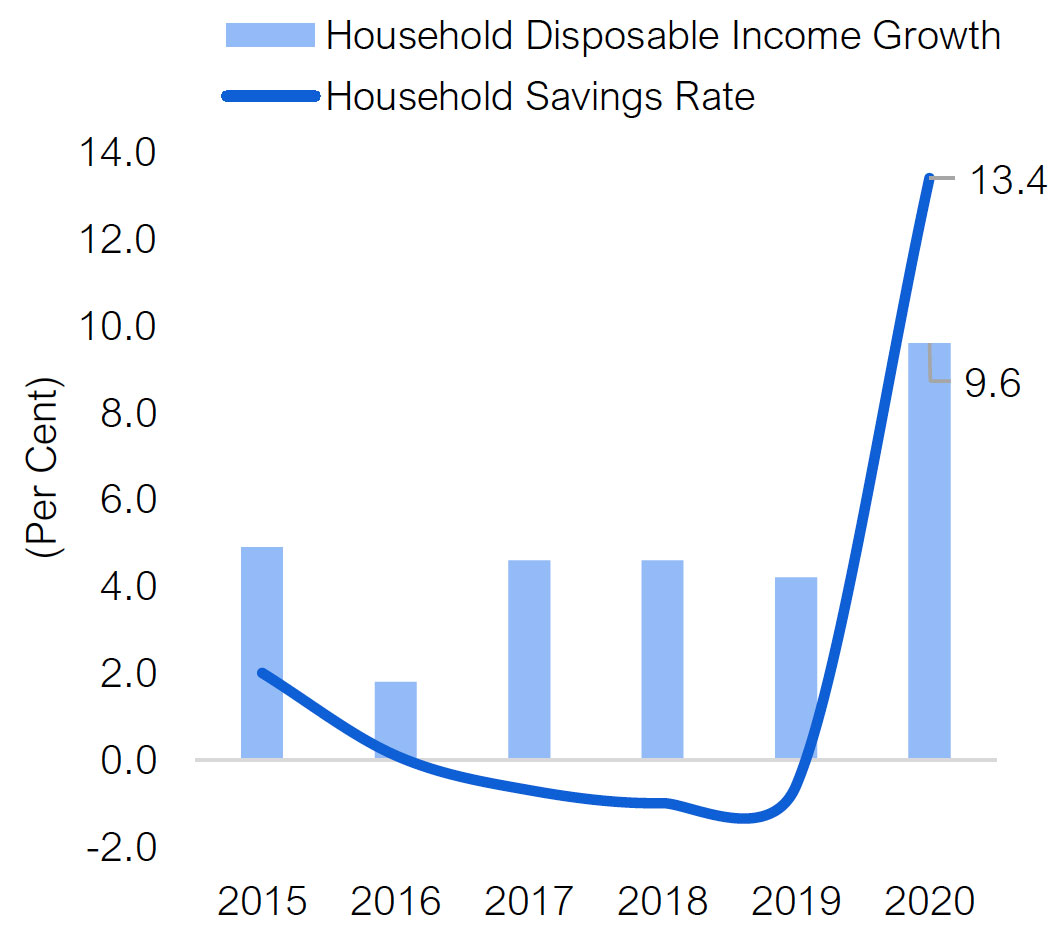

Rising employment will bolster labour income, which is projected to rebound strongly by 5.8 per cent in 2021. Significant income support from government, combined with reduced spending resulted in households saving a greater portion of their income, and the household savings rate[11] jumped from -0.6 per cent in 2019 to 13.4 per cent in 2020, the highest since 1993. As the economy fully reopens, households are expected to begin spending their excess savings, particularly in sectors most impacted by the pandemic, such as travel, accommodation, recreation and culture.[12]

Corporate profits are projected to rebound by 10.5 per cent in 2021 as businesses return to more normal levels of activity. In the first quarter of 2021, business sentiment rose to the highest point since 2018,[13] and is expected to continue to improve as consumer demand returns to pre-pandemic levels and the economic recovery broadens. For the industries hardest hit by the COVID-19 pandemic, recovery may happen more gradually until the economy is permanently and fully reopened. Overall, nominal GDP is expected to rise by 8.3 per cent in 2021 and 6.0 per cent in 2022.

Economic recovery faces uncertainty and risks

The path to economic recovery in 2021 depends heavily on the success of the federal and provincial governments’ plans for the COVID-19 vaccine distribution. Current levels of vaccine supply and the pace of distribution suggest that the risks from production setbacks and logistical challenges have eased. However, there are challenges related to the rise of variant COVID-19 cases, noncompliance with public health guidelines and vaccine hesitancy.

In the medium term, the Ontario economy continues to face downside risks from the lingering impact of the pandemic which could result in an uneven pace of recovery.[14] While government support measures have helped mitigate some of the disproportionate impacts of the pandemic on low-income households, income inequality and household debt may increase as these measures are phased out, exacerbating financial challenges for some groups. Similar to past recessions, the youth unemployment rate remains elevated at 20.7 per cent compared to 9.3 per cent for all age groups, and is expected to take longer to recover, potentially disadvantaging younger Ontarians in work experience and earnings.[15]

Pent-up demand, elevated household savings, supply chain challenges and the surge in housing market activity may lead to a faster than projected increase in consumer prices. The Bank of Canada expects inflation to temporarily surpass its two per cent target as the economy recovers.[16] However, if upward price pressures persist, households and businesses may face burdens from higher costs. In that case, the Bank would likely need to consider the different impacts policy decisions would have on containing inflationary pressures but potentially slowing economic growth.

4 | Medium-Term Budget Outlook

Overview

The FAO projects Ontario’s budget deficit will increase from $8.7 billion in 2019–20 to a record $35.8 billion in 2020–21, reflecting the severe impact of the COVID-19 pandemic. As the province recovers and the economy rebounds, rising revenues are expected to help lower the budget deficit to $11.1 billion by 2023–24. In contrast, the government projects an $18.7 billion deficit in 2023–24 (excluding the reserve) mainly due to its significantly weaker revenue outlook.[17]

Figure 4‑1: Ontario’s budget deficits projected to be smaller compared to the government’s plan

Note: Budget Balance is presented without the reserve.

Source: 2021 Ontario Budget and FAO.

Medium-term revenue outlook

Total revenue is expected to decline modestly by $1.6 billion in 2020–21 from 2019–20, despite the substantial drop in economic activity caused by the COVID-19 pandemic. While the pandemic caused a sharp decline in tax revenue[18] (-$6.5 billion) and ‘Other’ revenues[19] (-$3.5 billion) in 2020–21, this is largely offset by a significant $8.4 billion (32.9 per cent) increase in transfers from the federal government—primarily consisting of one-time COVID-related support.[20]

Figure 4‑2: Sharp declines in tax and ‘other’ revenues partly offset by temporary increase in federal transfers

Source: 2021 Ontario Budget and FAO.

In 2021–22, total revenue is expected to rebound by $4.9 billion (3.2 per cent) as the recovery in economic activity strengthens. Revenue growth in 2021–22 is tempered by the removal of one-time COVID-related funding from the federal government, offsetting some of the strong rebound in taxation revenue and ‘Other’ revenue.

Over the remainder of the medium-term (2022–23 to 2023–24) total revenue is expected to grow at an average annual rate of 4.3 per cent, consistent with the FAO’s outlook for economic growth.

Budget’s revenue forecast appears understated compared to economic growth

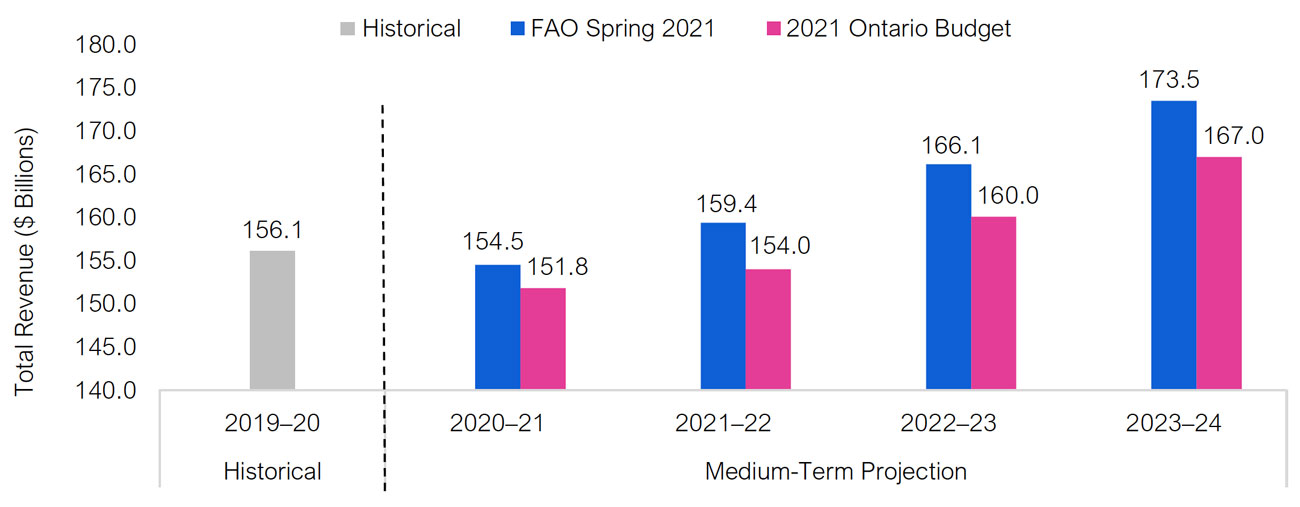

The FAO expects total revenues to be $2.7 billion higher in 2020–21 compared to the 2021 Ontario budget, with the difference growing over the medium term. By 2023–24, the FAO’s revenue forecast is $6.5 billion higher than the budget’s projection. This difference is largely because of the FAO’s forecast for stronger economic growth.

Figure 4‑3: FAO projects significantly higher revenues than Ontario budget

Source: 2021 Ontario Budget and FAO.

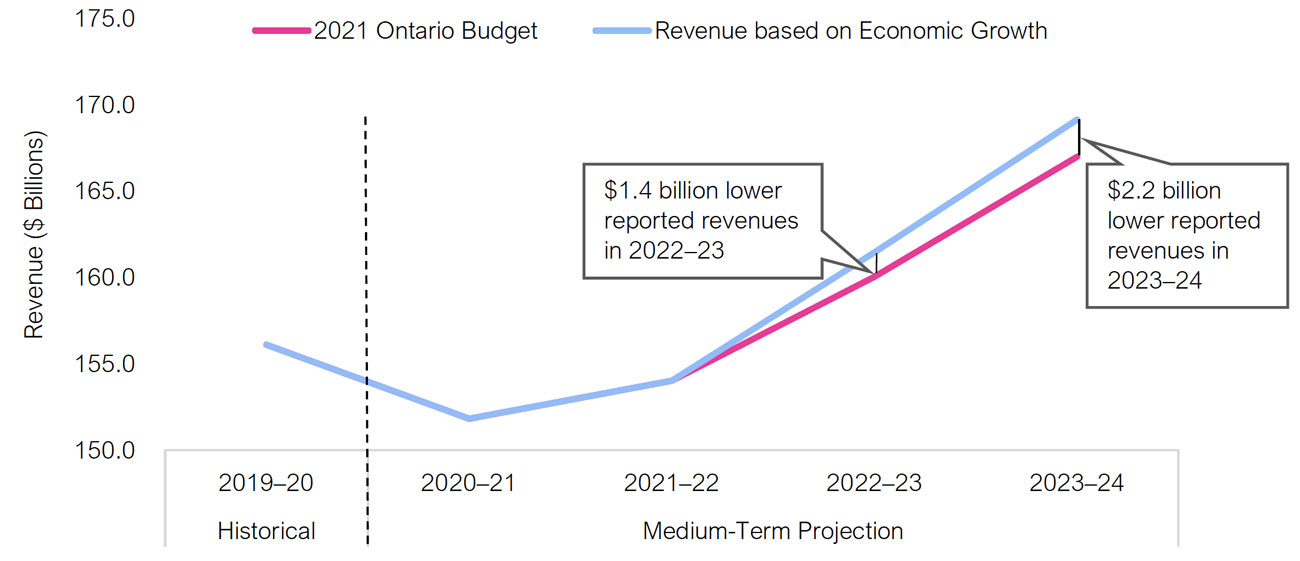

However, the budget’s revenue forecast is lower than what the government’s economic outlook would suggest. The FAO estimates that the budget’s revenue projection would be higher by about $1.4 billion in 2022–23 and $2.2 billion in 2023–24, based on the usual relationships between tax revenue and economic drivers.[21] Although not announced in the 2021 budget, these revenue shortfalls might be explained by potential planned tax cuts.[22] The FAO does not incorporate any unannounced tax changes into its revenue projection.

Figure 4‑4: Government projects lower revenues than economic growth in the budget suggests

Source: 2021 Ontario Budget and FAO.

Medium-term program expense outlook

The 2021 Ontario budget projects that program spending in 2020–21 will be $177.8 billion, or $25.6 billion higher than in 2019–20. This 16.8 per cent growth in program spending is the largest increase on record[23], mainly driven by temporary COVID-19 related spending.

Government plans to slow base program spending growth after 2021–22

Given the government’s general discretion over program spending, the FAO’s outlook incorporates the medium-term (2020–21 to 2023–24) spending plan from the 2021 Ontario budget. According to the plan, total program spending growth is projected to moderate over the medium term as temporary COVID-19 related measures are gradually phased out. Specifically, COVID-19 related spending is expected to decline from $20.1 billion in 2020–21 to $2.8 billion in 2022–23.

Base program spending growth, which excludes pandemic-related temporary expenses, increases significantly in 2021–22 and slows sharply afterwards.[24] In particular, base program spending is projected to grow by 3.9 per cent in 2020–21 and 5.4 per cent in 2021–22. However, growth in base program spending is expected to slow significantly to 2.1 per cent in 2022–23 and just 0.8 per cent in 2023–24.

Figure 4‑5: Base program spending growth projected to slow significantly after 2021–22

Source: 2021 Ontario Budget and FAO.

Planned program spending growth in key sectors will be significantly slower than the demand for public services

Planned program spending growth in the budget will not keep pace with the projected underlying demand for public services over the medium term. The FAO’s analysis suggests that for the government to achieve its medium-term spending plan, without breaching its commitment[25] to not introduce new cuts to spending, it would need to find savings of roughly $5 billion by 2023–24. Importantly, the 2021 budget has sufficient prudence in planned contingency funds combined with the reserve, to keep program spending in line with demand for services over the medium term. However, the government could choose to allocate these funds to reduce the budget deficit.

Planned program spending growth over the medium term is significantly lower than the expected demand for public services in most key sectors:

- Health: In the Health sector, planned program spending is projected to grow at an average annual pace of 3.1 per cent over the 2020–21 to 2023–24 period. This is slower than the 4.4 per cent growth in the FAO’s forecast that includes population growth, aging, and price inflation.[26]

- Education: In the Education sector, planned program spending is projected to grow at an average annual pace of 1.4 per cent, with significantly slower spending growth after 2021–22. This is below the FAO’s forecast of 1.9 per cent growth that includes school-age population growth, the number of children in childcare, and price inflation.[27]

- Postsecondary Education: In the Postsecondary Education sector, planned program spending is projected to grow at an average annual pace of 1.5 per cent, significantly below the 3.0 per cent growth in demand factors such as college and university enrollment, and price inflation.

- Children’s and Social Services: In the Children’s and Social Services sector, planned program spending is projected to grow at an average annual pace of 1.5 per cent, with spending slowing substantially after 2020–21. This is slower than the 2.5 per cent growth in demand factors such as the children and youth population, the number of beneficiaries in Ontario Disability Support and Ontario Works program, and price inflation.

- Justice: In the Justice sector, planned program spending is projected to grow at an average annual pace of just 0.3 per cent, the slowest among all sectors. This is substantially slower than the 2.0 per cent growth in demand factors such as the size of the police force, incarceration rates, the number of legal aid applications, court caseloads, and price inflation.

Figure 4‑6: Base program expense growth in key sectors will not keep pace with demand drivers

*FAO Spring 2021 program spending projection is adopted from the 2021 Ontario Budget.

Note: The average annual growth rates over the medium term in different sectors refer to base program spending and do not include any COVID-19 related spending.

Source: 2021 Ontario Budget and FAO.

Source: 2021 Ontario Budget and FAO.

Source: 2021 Ontario Budget and FAO.

Other Programs

‘Other Programs’ spending as presented in the budget is projected to grow at an average annual pace of 6.5 per cent over the medium term. As ‘Other Programs’ include a variety of ministries along with the standard operating and capital contingency funds, the FAO has broken down the category into ‘Other Ministries’ and ‘Contingency Funds’ components:

- Other Ministries: Planned program spending in other ministries [28] is projected to grow at an average annual pace of 3.8 per cent[29] over the medium term. Unlike the spending in key sectors, planned program spending in other ministries will surpass the expected 2.8 per cent average growth in key demand factors such as population and price inflation.

- Contingency Funds: In the 2021 budget, the government allocated $2.1 billion for standard contingency funds in 2021–22[30], nearly double the usual size of the funds,[31] and in addition to the dedicated COVID-19 contingency funds. After 2021–22, the amount of planned contingency funds is projected to remain significantly above its usual size.

Medium-term budget deficit outlook

The FAO projects a record budget deficit of $35.8 billion (or 4.2 per cent of GDP) in 2020–21, as the COVID-19 pandemic caused a small decline in revenues and a sharp increase in program spending. The 2021 budget projects a deficit of $38.5 billion in 2020–21, $2.7 billion higher compared to the FAO’s projection and mainly the result of the government’s lower revenue forecast.

Figure 4‑8: Ontario projected to record smaller budget deficits compared to the government’s outlook

The Budget Balance is presented without the reserve.

Source: 2021 Ontario Budget and FAO.

Ontario’s deficits are expected to improve over the medium term as the province recovers from the COVID-19 pandemic and the economy rebounds. The FAO projects that under current policies, Ontario’s deficit would decline from $26.5 billion in 2021–22 to $11.1 billion by 2023–24, a significant improvement but still larger than the $8.7 billion deficit recorded before the pandemic in 2019–20.

In contrast, the government’s deficit forecast improves much more slowly than the FAO’s projection. In 2021–22, the FAO expects a deficit of $26.5 billion, which is $5.6 billon smaller than the government’s $32.1 billion deficit projection. By 2023–24, the FAO projects a deficit of $11.1 billion, which is $7.6 billion smaller than the deficit projected by the government. The difference results from the FAO’s higher revenue projection ($6.5 billion higher in 2023–24) combined with a lower interest on debt forecast ($1.1 billion lower in 2023–24).

Medium-term net debt outlook

Net debt is expected to rise sharply in 2020–21, increasing by $43.5 billion to $396.8 billion. The substantial increase in net debt results in a large jump in the net debt-to-GDP ratio, which reaches 46.8 per cent in 2020–21. Even with stronger economic growth and declining deficits, the net debt-to-GDP ratio rises to 47.6 per cent in 2023–24, which is eight percentage points higher than the pre-pandemic ratio of 39.6 per cent in 2019–20.

Figure 4‑9: Net debt increases substantially in 2020–21 and over medium-term outlook

Source: Statistics Canada, Ontario Public Accounts and FAO.

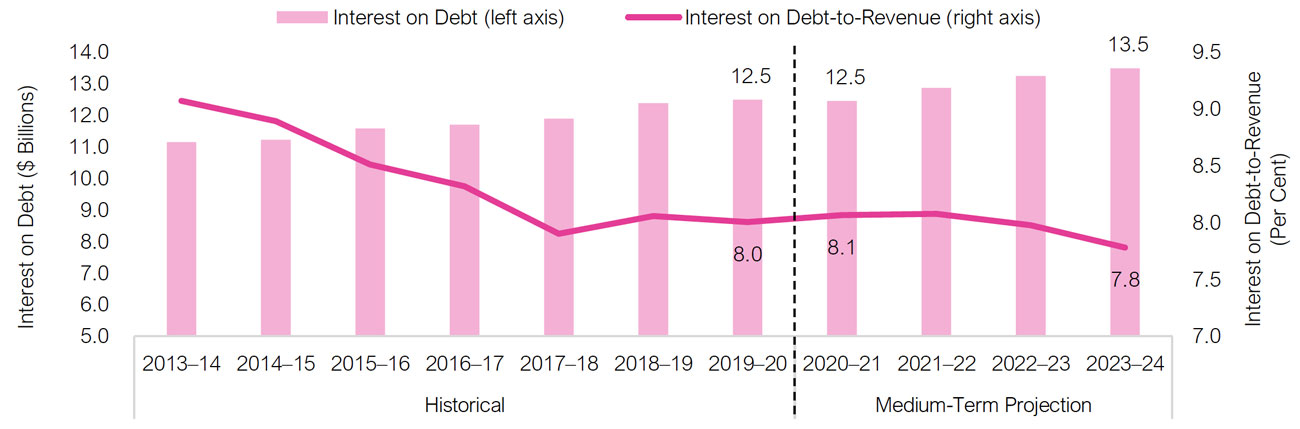

Despite the small increase in interest rates since the beginning of 2021, government borrowing rates remain near historic lows. These low borrowing rates are expected to limit the rise in interest on debt payments over the outlook.[32] By 2023–24, interest on debt is projected to reach $13.5 billion, a $1 billion increase from 2019–20, while net debt increases by $127.4 billion over the same period.

As a share of revenue, interest on debt is expected to rise modestly to 8.1 per cent in 2020–21, the result of low borrowing rates and the small decline in revenues. However, as revenues rebound, interest payments as a share of revenues are expected to decline gradually over the medium-term forecast, reaching 7.8 per cent by 2023–24, below the pre-pandemic (2019–20) share of 8.0 per cent. Despite the significant increase in borrowing, the share of revenue that must be directed to interest payments declines through 2023–24, implying a larger portion of revenue could potentially be allocated towards program spending.[33]

Figure 4‑10: Interest on debt to rise slowly over medium-term projection

Source: Ontario Public Accounts and FAO.

5 | Ontario’s Fiscal Recovery Plan

According to Ontario’s Fiscal Sustainability, Transparency and Accountability Act 2019 (FSTAA), the government is required to present a recovery plan to balance the budget if there is a deficit by the end of the current multi-year plan.[34] In the 2021 Ontario budget, the government presented a recovery plan that projected a path to a balanced budget by 2029–30. However, the government’s recovery plan relies on prolonged spending restraint that would require significant and permanent cost savings that have historically been difficult to achieve.[35] The budget does not provide details on how the government would be able to accomplish the savings implied by their spending plan.

To assess the government’s plan, the FAO developed an independent fiscal projection over the recovery period, incorporating a revenue and program spending outlook based on economic and demographic factors. According to the FAO’s projection, Ontario is not expected to achieve a balanced budget by 2029–30. In contrast to the government’s projection of a $2.4 billion surplus in 2029–30, the FAO expects the province to have a deficit of $6.9 billion, under current policies.

Figure 5‑1: Ontario’s budget will not be balanced by 2029–30

Note: Budget Balance is presented before the reserve.

Source: 2021 Ontario Budget and FAO.

To eliminate the $6.9 billion deficit in 2029–30 projected by the FAO, a number of policy actions could be taken. See Table C‑3 in the Appendix for estimates of both the immediate impact in 2021–22 as well as the longer-term impact in 2029–30 of various policy changes on the budget.

Recovery Plan revenue outlook

The FAO expects total revenue to grow by an average of 3.5 per cent per year over the recovery plan, in line with its projection of economic growth. This outlook is based on existing tax rates and a continuation of current federal transfers agreements. In 2029–30, the FAO’s revenue forecast is $3.6 billion above the budget’s outlook, reflecting the FAO’s significantly stronger revenue growth in the medium term.

Figure 5‑2: FAO projects higher revenues than Budget during recovery

Source: 2021 Ontario Budget and FAO.

Recovery Plan expense outlook

Based on the 2021 Ontario budget, the government’s program spending is projected to grow at an average annual rate of 1.5 per cent over the recovery plan (2024–25 to 2029–30). The government has indicated that their spending plan is based on cost saving efficiencies in the delivery of public services, rather than cuts to existing programs. However, the Budget does not explain how these efficiencies will be achieved.

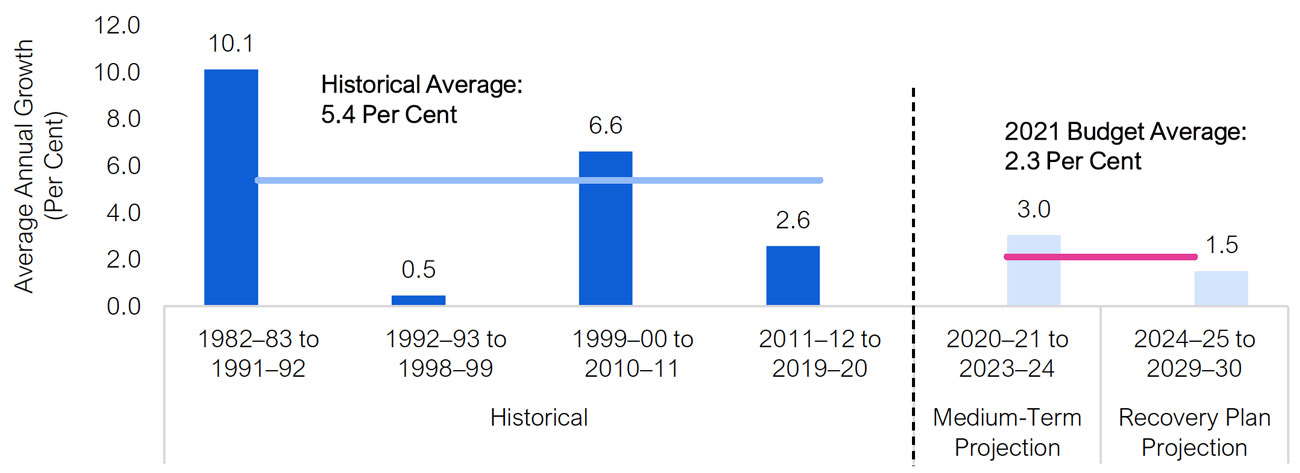

Sustained transformation to the delivery of public services resulting in permanent cost savings have been historically difficult to achieve.[36] In the past, long periods of spending restraint resulted in lengthy periods of stronger “catch-up” spending growth as unaddressed pressures emerge, as shown in Figure 5-3.

Figure 5‑3: Government’s Recovery Plan relies on significantly limiting program spending growth

Source: Ontario Public Accounts, 2021 Ontario Budget and FAO.

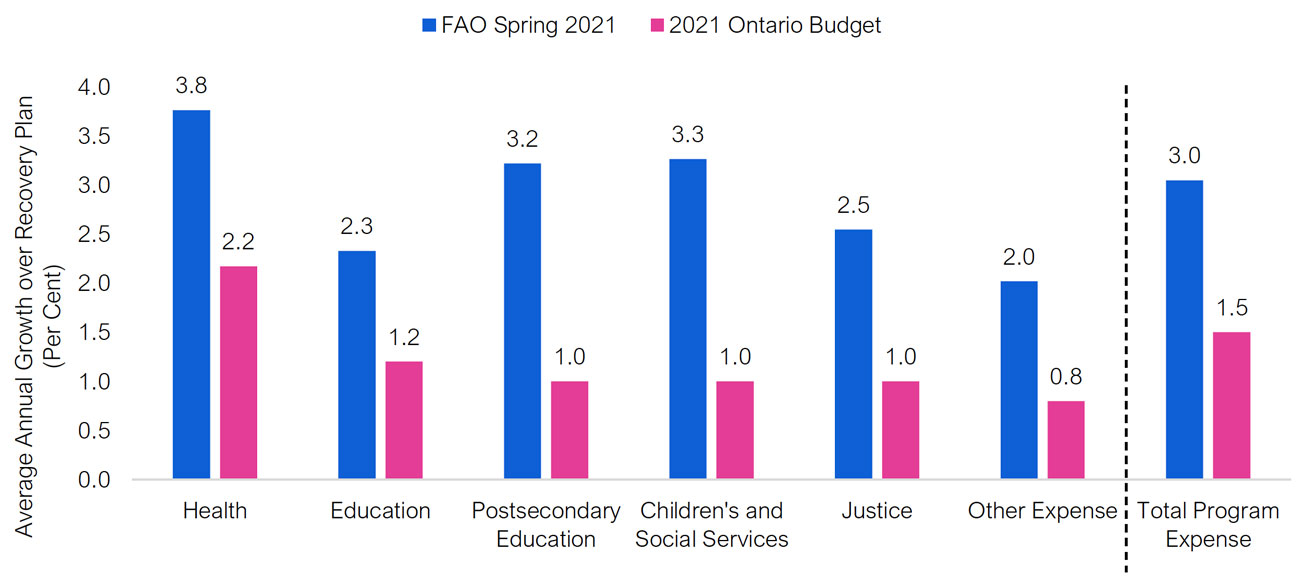

To assess the government’s spending growth projection in the recovery plan, the FAO developed a spending projection based on demand drivers for each sector.[37] On this basis, program spending is expected to grow by an average of 3.0 per cent annually — twice the pace of the government’s planned spending growth of 1.5 per cent over the recovery plan period. According to the FAO’s outlook, the government’s planned spending growth is significantly below expected demand for public services in all major programs, including health[38] and education[39].

Figure 5‑4: Program spending to outpace planned growth over the recovery period

Source: 2021 Ontario Budget and FAO.

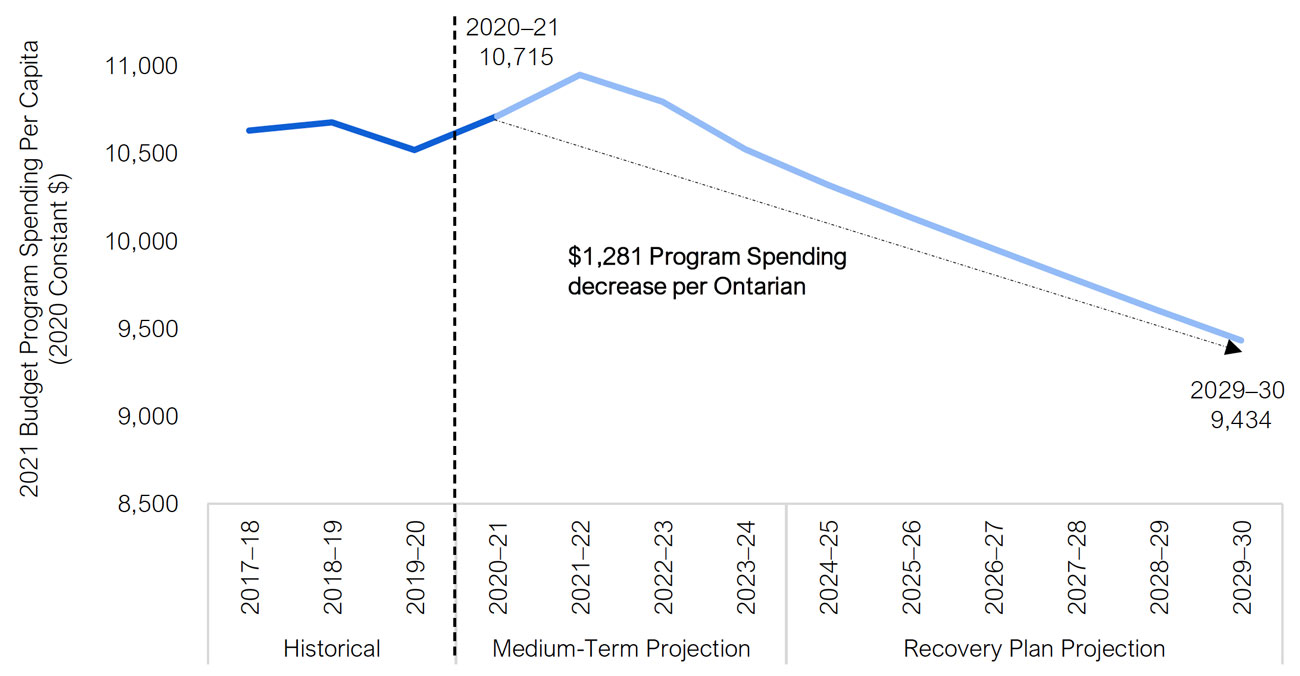

By the end of the recovery plan, the FAO’s outlook for program spending is $17.8 billion higher than the government’s recovery plan in the 2021 budget. To achieve its recovery plan, the government would have to introduce new program changes that lower spending by $1,281 per Ontarian by 2029–30 in 2020 dollars.

Figure 5‑5: Planned program spending per Ontarian decreases $1,281 by 2029–30

Source: Ontario Public Accounts, Statistics Canada, 2021 Ontario Budget and FAO.

6 | Fiscal Sustainability

In the 2021 budget, the government presented a target for the net debt-to-GDP ratio to not exceed 50.5 per cent over the medium term and committed to slow the rate of increase in net debt-to-revenue and interest on debt-to-revenue. In addition, the government presented a path to balance the budget in 2029–30 in its recovery plan.[40]

To assess the state of the government’s finances over the 2020–21 to 2029–30 period, the FAO evaluated several fiscal indicators. Figure 6-1 presents the trends in these key indicators historically and over the recovery period. Based on this assessment, the FAO finds:

- With ongoing demand for public services, program spending is expected to exceed the government’s forecast significantly. However, projected revenues will be more than sufficient to cover program expense, leading to increasing primary surpluses over the recovery period.

- The government is not expected to balance its budget by 2029–30 under current policies. Even so, with revenues rising faster than program spending and interest expense, the overall budget deficit as a share of GDP will decline steadily over the recovery period.

- Despite the large ongoing deficits, primary surpluses will lower the borrowing requirement of the government as some revenue will be available to pay for debt interest costs—tempering the rise in net debt over the recovery period. Given the expected pace of economic growth, the net debt-to-GDP ratio will continue to decline modestly and remain below the government’s target throughout the projection.

- Increasing debt levels and gradually rising borrowing rates will lead to higher interest on debt payments. However, with revenues projected to grow at a faster rate, the FAO expects that the interest on debt-to-revenue ratio will decline gradually over the recovery plan, providing the government slightly more budgetary flexibility.

Ontario’s finances vulnerable to several risks

The consistent improvement in Ontario’s fiscal indicators is driven by the assumptions that there will be no change in fiscal policy, and economic growth will exceed the province’s effective borrowing rate. However, this progress could be hindered if interest rates rise above expected economic growth. In that case, net debt would grow faster than the economy, potentially pushing the province’s debt burden above the government’s target. It would also result in interest on debt-to-revenue increasing faster, impeding the government’s commitment to slow the rate of increase in the ratio.

Changes in fiscal policy, such as tax cuts, may reduce the projected primary surplus, which would increase the government’s borrowing requirement, and significantly delay the improvements in fiscal indicators.

There are other factors that could result in further progress in the government’s fiscal targets, including stronger than expected economic growth and successful program transformation that allows the government to lower expenses without impacting the delivery or quality of public services.

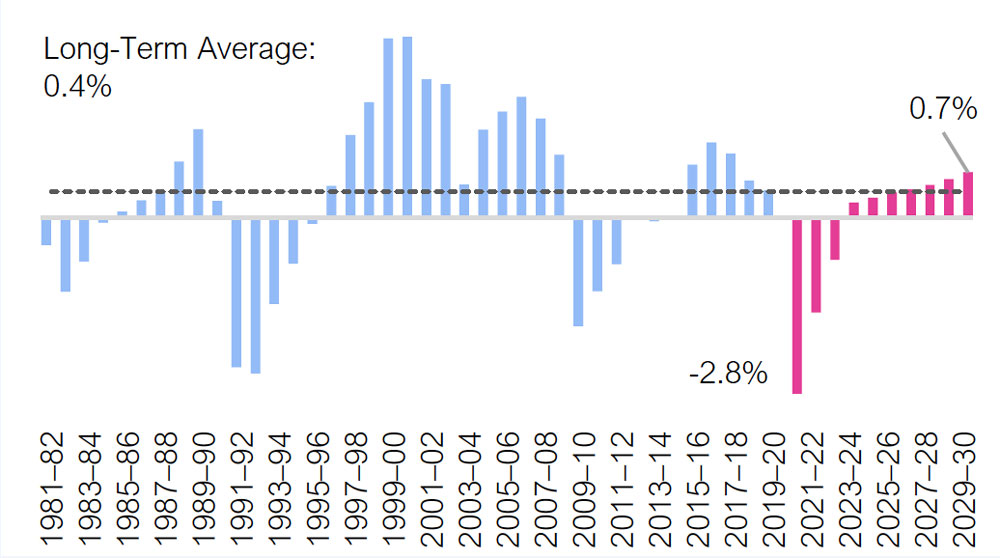

Figure 6‑1: Trends in key deficit and debt indicators for Ontario

Primary Budget Balance as a share of GDP

- The primary budget balance measures the extent to which program spending is being funded from current revenues and shows the component of public finances most under the control of the government.

- Historically averaged a surplus of 0.4 per cent of the province’s GDP.

- Projected to deteriorate to a deficit of -2.8 per cent of GDP in 2020–21, and record increasing surplus starting in 2023–24, surpassing the long-term average in 2026–27.

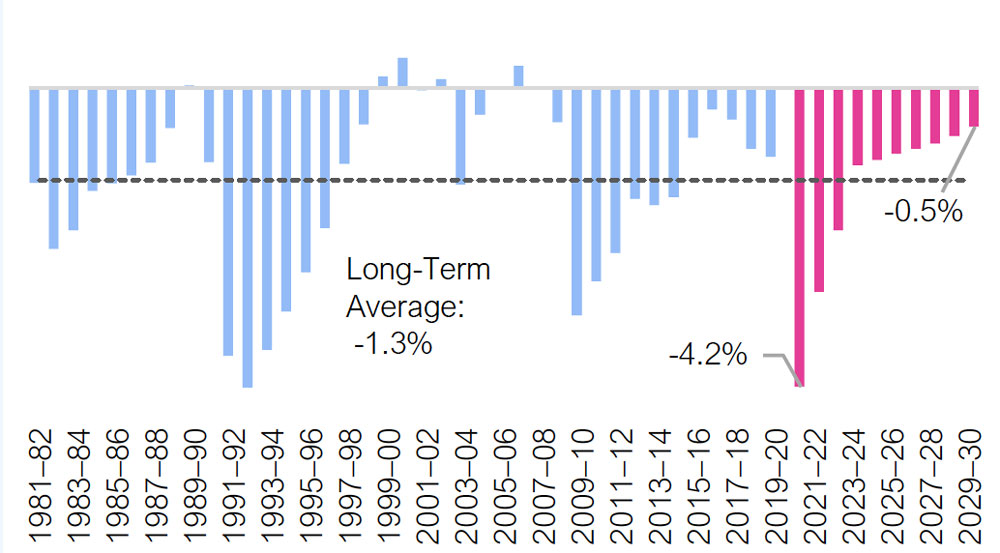

Overall Budget Balance as a share of GDP

- The overall budget balance measures the extent to which the government needs to borrow to cover its program expense and interest payments. Under FSTAA, the government is required to release a plan for an overall balanced budget when in deficit.

- Historically averaged a deficit of -1.3 per cent of GDP, deteriorating during economic downturns and improving in recoveries.

- Projected to fall to a deficit of -4.2 per cent in 2020–21 and improve gradually over the projection – surpassing the long-term average deficit in 2023–24, but not reaching balance.

Net Debt as a share of GDP

- Net debt as a share of GDP indicates the ability of the government to raise funds to repay its debt obligations. Under FSTAA, the government is required to present a debt burden reduction strategy in its annual budget.

- Historically averaged 26.8 per cent of GDP, but has progressively increased over the past four decades, rising noticeably during economic downturns.

- Projected to reach a record 47.6 per cent in 2023–24 and decline to 44.7 per cent by 2029–30.

Interest on Debt as a share of revenue

- The ratio of interest on debt-to-revenue indicates budgetary flexibility – a higher ratio means the government has less revenue available to spend on key programs such as health care or education.

- Historically averaged 10.3 per cent of revenues.

- Projected to decline gradually from 8.1 per cent in 2020–21 to 7.3 per cent by 2029–30.

Source: Ontario Economic Accounts, Ontario Public Accounts, 2021 Ontario Budget and FAO.

7 | Appendix

Appendix A : Economic Tables

(Per Cent Growth)

2019a

2020a

2021f

2022f

2023f

2024f

2025f

Nominal GDP

FAO - Spring 2021

3.8

-4.8

8.3

6.0

3.7

3.4

3.4

2021 Ontario Budget*

3.8

-4.8

6.2

6.4

4.5

4.0

-

Consensus**

3.8

-4.8

8.0

6.2

4.4

4.1

4.2

Labour Income

FAO - Spring 2021

4.6

-1.3

5.8

4.6

3.6

3.3

3.3

2021 Ontario Budget

4.6

-1.3

4.2

5.0

4.8

4.1

-

Corporate Profits

FAO - Spring 2021

0.0

-9.9

10.5

7.7

4.2

3.7

3.7

2021 Ontario Budget

0.0

-9.9

8.0

7.4

4.4

4.2

-

Household Consumption

FAO - Spring 2021

3.5

-6.0

8.1

6.1

3.8

3.7

3.6

2021 Ontario Budget

3.5

-6.0

5.9

7.2

4.9

4.2

-

* Ministry of Finance forecast released in the 2021 Ontario Budget was based on information available up to February 3, 2021.

** Composed of private-sector banks and forecasters. Forecasts as of June 4, 2021.

Source: Ontario Economic Accounts, 2021 Ontario Budget and FAO.

(Per Cent Growth)

2019a

2020a

2021f

2022f

2023f

2024f

2025f

Real GDP

FAO - Spring 2021

2.1

-5.8

5.8

4.0

2.0

1.7

1.7

2021 Ontario Budget

2.1

-5.8

4.0

4.3

2.5

2.0

-

Consensus**

2.1

-5.8

5.3

4.2

2.5

2.2

2.1

Real GDP Components

Household Consumption

1.9

-6.1

4.8

3.8

1.9

1.6

1.6

Residential Investment

0.5

7.9

11.0

4.8

2.3

1.8

1.8

Business Investment

-2.6

-12.5

4.1

4.4

1.8

1.6

1.6

Government (Consumption and Investment)

1.3

-1.4

4.6

2.0

2.0

2.0

2.0

Exports

2.1

-8.7

7.4

4.2

2.2

1.8

1.8

Imports

0.6

-9.2

9.5

4.1

2.1

1.8

1.8

* Ministry of Finance forecast released in the 2021 Ontario Budget was based on information available up to February 3, 2021.

** Composed of private-sector banks and forecasters. Forecasts as of June 4, 2021.

Source: Ontario Economic Accounts, 2021 Ontario Budget and FAO.

(Per Cent Growth)

2019a

2020a

2021f

2022f

2023f

2024f

2025f

Employment

FAO - Spring 2021

2.8

-4.8

5.0

3.2

1.6

1.2

1.2

2021 Ontario Budget*

2.8

-4.8

4.2

3.0

2.2

1.6

-

Unemployment Rate (Per Cent)

FAO - Spring 2021

5.6

9.6

7.9

6.8

6.4

6.2

6.0

2021 Ontario Budget

5.6

9.6

8.2

6.9

6.5

6.3

-

Labour Force

FAO - Spring 2021

2.7

-0.6

3.1

2.0

1.2

0.9

0.9

2021 Ontario Budget

-

-

-

-

-

-

-

CPI Inflation (Per Cent)

FAO - Spring 2021

1.9

0.7

2.5

2.2

2.0

2.0

2.0

2021 Ontario Budget

1.9

0.7

1.7

2.0

2.0

2.0

-

Canada Real GDP

FAO - Spring 2021

1.9

-5.4

5.9

4.0

2.2

1.9

1.9

2021 Ontario Budget

-

-

-

-

-

-

-

U.S. Real GDP

FAO - Spring 2021

2.2

-3.5

6.4

4.0

2.3

2.0

1.9

2021 Ontario Budget

2.2

-3.5

4.9

3.8

2.3

2.1

-

Canadian Dollar (Cents US)

FAO - Spring 2021

75.4

74.6

80.1

79.1

79.1

79.1

79.0

2021 Ontario Budget

75.4

74.6

78.5

78.5

79.2

80.2

-

Three-month Treasury Bill Rate (Per Cent)

FAO - Spring 2021

1.7

0.4

0.1

0.2

0.4

0.9

1.4

2021 Ontario Budget

1.7

0.4

0.2

0.2

0.5

1.1

-

10-year Government Bond Rate (Per Cent)

FAO - Spring 2021

1.6

0.7

1.6

1.8

2.1

2.3

2.4

2021 Ontario Budget

1.6

0.7

1.0

1.4

1.8

2.4

-

* Ministry of Finance forecast released in the 2021 Ontario Budget was based on information available up to February 3, 2021.

Source: Statistics Canada, 2021 Ontario Budget and FAO.

Appendix B : Medium-Term Fiscal Tables

($ Billions)

2017–18a

2018–19a

2019–20a

2020–21f

2021–22f

2022–23f

2023–24f

Revenue

Personal Income Tax

32.9

35.4

37.7

38.1

38.8

40.7

42.5

Sales Tax

25.9

27.8

28.6

26.3

29.5

31.7

33.0

Corporations Tax

15.6

16.6

15.4

10.5

12.6

13.3

14.1

All Other Taxes

25.3

25.7

26.5

26.8

29.3

29.1

29.9

Total Taxation Revenue

99.7

105.5

108.3

101.8

110.2

115.0

119.6

Transfers from Government of Canada

24.9

25.1

25.4

33.7

27.4

27.7

28.8

Income from Government Business Enterprise

6.2

5.5

5.9

3.9

4.5

5.5

6.6

Other Non-Tax Revenue

19.9

17.6

16.5

15.1

17.2

18.0

18.5

Total Revenue

150.6

153.7

156.1

154.5

159.4

166.1

173.5

Expense

Health Sector

59.1

61.9

63.7

75.2

74.9

72.6

72.0

Health (Base)

59.1

61.9

63.7

66.7

69.8

70.6

72.0

Temporary COVID-19 Funds

0.0

8.4

5.1

2.0

0.0

Education Sector

27.3

28.7

30.2

32.1

31.3

31.4

31.5

Education (Base)

27.3

28.7

29.8

30.6

31.3

31.4

31.5

Temporary COVID-19 Funds

0.4

1.6

0.1

0.0

0.0

Children's and Social Services Sector

16.2

16.8

17.1

17.8

17.9

18.0

18.1

Children's and Social Services (Base)

16.2

16.8

17.1

17.7

17.8

18.0

18.1

Temporary COVID-19 Funds

0.0

0.1

0.1

0.0

0.0

Postsecondary Education Sector

10.5

11.2

10.5

10.3

10.7

11.0

11.2

Postsecondary Education (Base)

10.5

11.2

10.5

10.3

10.7

11.0

11.2

Temporary COVID-19 Funds

0.0

0.0

0.0

0.0

0.0

Justice Sector

4.3

4.4

4.7

4.7

4.8

4.8

4.7

Justice (Base)

4.3

4.4

4.7

4.6

4.8

4.8

4.7

Temporary COVID-19 Funds

0.0

0.1

0.0

0.0

0.0

Other Programs

25.0

25.7

26.1

37.8

33.4

34.8

33.5

Other*(Base)

25.0

25.7

26.1

27.8

31.9

34.0

33.5

Temporary COVID-19 Funds

>0.1

10.0

1.4

0.8

0.0

Total Program Expense

142.4

148.8

152.3

177.8

173.0

172.5

171.1

Total Program Expense (Base)

142.4

148.8

151.8

157.7

166.3

169.7

171.1

Total Temporary COVID-19 Funds

0.5

20.1

6.7

2.8

0.0

Interest on Debt

11.9

12.4

12.5

12.5

12.9

13.3

13.5

Total Expense

154.3

161.1

164.8

190.3

185.9

185.8

184.6

Budget Balance**

-3.7

-7.4

-8.7

-35.8

-26.5

-19.6

-11.1

*Includes Teachers’ Pension Plan.

**Budget Balance is presented without reserve.

Numbers may not add due to rounding.

Source: Statistics Canada, Ontario Economic Accounts, Ontario Public Accounts, 2021 Ontario Budget and FAO.

($ Billions)

2017–18a

2018–19a

2019–20a

2020–21f

2021–22f

2022–23f

2023–24f

Budget Balance*

-3.7

-7.4

-8.7

-35.8

-26.5

-19.6

-11.1

Accumulated Deficit

209.0

216.6

225.8

261.6

288.1

307.7

318.8

Net Debt

323.8

338.5

353.3

396.8

431.6

461.0

480.8

Net Debt-to-GDP (Per Cent)

39.3

39.4

39.6

46.8

47.0

47.3

47.6

*Budget Balance is presented without reserve.

Numbers may not add due to rounding.

Source: Statistics Canada, Ontario Economic Accounts, Ontario Public Accounts, 2021 Ontario Budget and FAO.

Appendix C : Recovery Plan Outlook

2019a

2020f

2021f

2022f

2023f

2024-30f

Nominal GDP (Per Cent Growth)

3.8

-4.8

8.3

6.0

3.7

3.7

Three-month Treasury Bill Rate (Per Cent)

1.7

0.4

0.1

0.2

0.4

1.6

10-year Government Bond Rate (Per Cent)

1.6

0.7

1.6

1.8

2.1

2.7

Effective Interest Rate (Per Cent)

3.4

3.4

3.0

2.9

2.9

2.9

Historical

Medium-term Projection

Recovery Period Projection

2019–20a

2020–21f

2021–22f

2022–23f

2023–24f

2024–25f

2025–26f

2026–27f

2027–28f

2028–29f

2029–30f

Revenue

156.1

154.5

159.4

166.1

173.5

179.5

185.6

192.2

199.0

206.2

213.7

Total Program Expense

152.3

177.8

173.0

172.5

171.1

176.3

181.4

187.2

193.1

199.0

204.8

Interest on Debt

12.5

12.5

12.9

13.3

13.5

13.9

14.3

14.7

15.1

15.4

15.7

Total Expense

164.8

190.3

185.9

185.8

184.6

190.2

195.7

201.8

208.2

214.4

220.5

Interest on Debt as a Share of Revenue (Per Cent)

8.0

8.1

8.1

8.0

7.8

7.7

7.7

7.6

7.6

7.5

7.3

Budget Balance*

-8.7

-35.8

-26.5

-19.6

-11.1

-10.7

-10.0

-9.7

-9.1

-8.2

-6.9

Net Debt

353.3

396.8

431.6

461.0

480.8

493.8

510.1

526.6

541.6

553.6

560.9

Net Debt-to-GDP (Per Cent)

39.6

46.8

47.0

47.3

47.6

47.3

47.2

47.0

46.5

45.8

44.7

*Budget Balance is presented without reserve.

Numbers may not add due to rounding.

Source: Statistics Canada, Ontario Economic Accounts, Ontario Public Accounts, 2021 Ontario Budget and FAO.

Change in budget balance in:

Change Beginning in 2021–22

2021–22

2029–30

Tax Policy

A sustained 10 per cent increase in Personal Income Tax revenues ($500 per tax filer in 2020–21) over the projection

+$4.0 billion

+$7.0 billion

A sustained one percentage point increase in Corporations Tax rates over the projection[41]

+$1.0 billion

+$1.7 billion

A sustained one percentage point increase in the HST rate over the projection

+$3.8 billion

+$6.6 billion

Federal Transfers

A sustained one percentage point increase in the annual growth of the Canada Health Transfer over the projection

+$0.3 billion

+$2.8 billion

A sustained one percentage point increase in the annual growth of the Canada Social Transfer over the projection

+$0.1 billion

+$0.9 billion

Expenditure Policy

A sustained 0.5 percentage point decrease in the growth rate of total program spending over the projection

+$0.9 billion

+$9.0 billion

A sustained one percentage point decrease in the growth rate of health spending over the projection

+$0.7 billion

+$7.7 billion

Source: FAO.

About this document

Established by the Financial Accountability Officer Act, 2013, the Financial Accountability Office (FAO) provides independent analysis on the state of the Province’s finances, trends in the provincial economy and related matters important to the Legislative Assembly of Ontario.

This report was prepared by Sabrina Afroz, Zohra Jamasi, Jay Park and Nicolas Rhodes, under the direction of Edward Crummey and Paul Lewis. External reviewers were provided with earlier drafts of this report for their comments. However, the input of external reviewers implies no responsibility for this final report, which rests solely with the FAO.

The content of this report is based on information available to June 4, 2021. Background data used in this report are available upon request.

In keeping with the FAO’s mandate to provide the Legislative Assembly of Ontario with independent economic and financial analysis, this report makes no policy recommendations.

FAO’s Fiscal Projections

The FAO forecasts provincial finances based on projections of existing and announced revenue and spending policies. The FAO’s tax revenue projections are based on an assessment of the outlook for the provincial economy and current tax policies. All average annual growth rates in this report are calculated using the year before the first indicated year as the base.

Graphic Descriptions

Historical

Medium-term Projection

Ontario GDP Growth (Per Cent)

2019

2020

2021

2022

2023

2024

2025

Real

2.1

-5.8

5.8

4.0

2.0

1.7

1.7

Average Annual Growth over Medium-Term

(Per Cent)

FAO Spring 2021 (Adopted from Budget)

Demand Drivers

Health

3.1

4.4

Education

1.4

1.9

Postsecondary Education

1.5

3.0

Children’s and Social Services

1.5

2.5

Justice

0.3

2.0

Historical

Medium-term Projection

Budget Balance ($ Billions)

2017-18

2018-19

2019-20

2020-21

2021-22

2022-23

2023-24

Historical

-3.7

-7.4

-8.7

FAO Spring 2021

-35.8

-26.5

-19.6

-11.1

2021 Ontario Budget

-38.5

-32.1

-26.2

-18.7

Budget Balance ($ Billions)

Historical

FAO Spring 2021

2021 Ontario Budget

Historical

2019-20

-8.7

Medium-Term Projection

2020-21

-35.8

-38.5

2021-22

-26.5

-32.1

2022-23

-19.6

-26.2

2023-24

-11.1

-18.7

Recovery Plan Projection

2024-25

-10.7

-15.7

2025-26

-10.0

-12.7

2026-27

-9.7

-9.7

2027-28

-9.1

-6.0

2028-29

-8.2

-2.1

2029-30

-6.9

2.4

Historical

Projection

Ontario GDP Growth

(Per Cent)

2019

2020

2021

2022

2023

2024

2025

Real

2.1

-5.8

5.8

4.0

2.0

1.7

1.7

Nominal

3.8

-4.8

8.3

6.0

3.7

3.4

3.4

Real GDP Growth (Per Cent)

World

Advanced

Economies

Emerging Market and

Developing Economies

Historical

2016

3.3

1.8

4.5

2017

3.8

2.5

4.8

2018

3.6

2.3

4.5

2019

2.8

1.6

3.6

Projection

2020

-3.3

-4.7

-2.2

2021

6.0

5.1

6.7

2022

4.4

3.6

5.0

2023

3.5

1.8

4.7

2024

3.4

1.6

4.6

2025

3.3

1.5

4.5

Historical

Projection

(Per Cent)

2018

2019

2020

2021

2022

2023

2024

2025

3-month Treasury Bill Yield

1.4

1.7

0.4

0.1

0.2

0.4

0.9

1.4

10-year Government of Canada Bond Yield

2.3

1.6

0.7

1.6

1.8

2.1

2.3

2.4

Real GDP ($2012 chained millions)

Historical

Projection

Historical

2019Q3

801556

2019Q4

802562

2020Q1

787704

2020Q2

691682

2020Q3

756993

2020Q4

772799

Projection

2021Q1

776865

2021Q2

787710

2021Q3

804684

2021Q4

814371

2022 Q1

822519

2022 Q2

826926

2022 Q3

829079

2022 Q4

833595

2023 Q1

839028

2023 Q2

842666

2023 Q3

846493

2023 Q4

849289

Year

Month

Thousands

2020

January

7,494.1

February

7,491.1

March

7,098.2

April

6409.9

May

6356.4

June

6,725.6

July

6,884.5

August

7,006.8

September

7,168.9

October

7,200.6

November

7,238.3

December

7,239.0

2021

January

7,085.5

February

7,185.8

March

7,368.1

April

7,215.4

May

7,183.8

Historical

Projection

2019

2020

2021

2022

2023

2024

2025

Employment Change (Thousands)

203.6

-355.3

350.8

238.8

119.0

90.9

90.3

Unemployment Rate (Per Cent)

5.6

9.6

7.9

6.8

6.4

6.2

6.0

Household Disposable Income Growth (Per Cent)

2015

2016

2017

2018

2019

2020

Household Disposable Income

Growth (Per Cent)

4.9

1.8

4.6

4.6

4.2

9.6

Household Savings Rate

2.0

0.1

-0.7

-1.0

-0.6

13.4

Historical

Medium-Term Projection

Budget Balance ($ Billions)

2017-18

2018-19

2019-20

2020-21

2021-22

2022-23

2023-24

Historical

-3.7

-7.4

-8.7

FAO Spring 2021

-35.8

-26.5

-19.6

-11.1

2021 Ontario Budget

-38.5

-32.1

-26.2

-18.7

Change in Revenue ($ Billions)

2020-21

2021-22

Tax Revenue

-6.5

8.4

Federal Transfers

8.4

-6.3

Other Revenue

-3.5

2.8

Total

-1.6

4.9

Historical

Medium-Term Projection

2019-20

2020-21

2021-22

2022-23

2023-24

Total Revenues ($ Billions)

156.1

154.5

159.4

166.1

173.5

Total Revenues ($ Billions)

Historical

Medium-Term Projection

2019-20

2020-21

2021-22

2022-23

2023-24

Historical

156.1

FAO Spring 2021

154.5

159.4

166.1

173.5

2021 Ontario Budget

151.8

154.0

160.0

167.0

Total Revenues ($ Billions)

Historical

Medium-Term Projection

2019-20

2020-21

2021-22

2022-23

2023-24

Revenue based on Economic Growth

156.1

151.8

154.0

161.4

169.1

2021 Ontario Budget

151.8

154.0

160.0

167.0

2020-21

2021-22

2022-23

2023-24

Average Annual Growth over Medium-Term (Per Cent)

3.9

5.4

2.1

0.8

Average Annual Growth over Medium-Term

(Per Cent)

FAO Spring 2021 (Adopted from Budget)

Demand Drivers

Health

3.1

4.4

Education

1.4

1.9

Postsecondary Education

1.5

3.0

Children’s and Social Services

1.5

2.5

Justice

0.3

2.0

Average Annual Growth over Medium-Term (Per Cent)

2021 Ontario Budget: Other Ministries & Contingency Funds

6.5

2021 Ontario Budget: Other Ministries

3.8

Demand Drivers

2.8

Historical

Medium-Term Projection

Budget Balance ($ Billions)

2017-18

2018-19

2019-20

2020-21

2021-22

2022-23

2023-24

Historical

-3.7

-7.4

-8.7

FAO Spring 2021

-35.8

-26.5

-19.6

-11.1

2021 Ontario Budget

-38.5

-32.1

-26.2

-18.7

Net Debt

($ Billions)

Net Debt-to-GDP Ratio

(Per Cent)

Historical

2013-14

276.2

39.7

2014-15

294.6

40.5

2015-16

306.4

40.3

2016-17

314.1

39.7

2017-18

323.8

39.3

2018-19

338.5

39.4

2019-20

353.3

39.6

Medium-Term Projection

2020-21

396.8

46.8

2021-22

431.6

47.0

2022-23

461.0

47.3

2023-24

480.8

47.6

Interest on Debt

($ Billions)

Interest on Debt-to-Revenue

(Per Cent)

Historical

2013-14

11.2

9.1

2014-15

11.2

8.9

2015-16

11.6

8.5

2016-17

11.7

8.3

2017-18

11.9

7.9

2018-19

12.4

8.1

2019-20

12.5

8.0

Medium-Term Projection

2020-21

12.5

8.1

2021-22

12.9

8.1

2022-23

13.3

8.0

2023-24

13.5

7.8

Budget Balance ($ Billions)

Historical

FAO Spring 2021

2021 Ontario Budget

Historical

2019-20

-8.7

Medium-Term Projection

2020-21

-35.8

-38.5

2021-22

-26.5

-32.1

2022-23

-19.6

-26.2

2023-24

-11.1

-18.7

Recovery Plan Projection

2024-25

-10.7

-15.7

2025-26

-10.0

-12.7

2026-27

-9.7

-9.7

2027-28

-9.1

-6.0

2028-29

-8.2

-2.1

2029-30

-6.9

2.4

Total Revenue ($ Billions)

Historical

FAO Spring 2021

2021 Ontario Budget

Historical

2019-20

156.1

Medium-Term Projection

2020-21

154.5

151.8

2021-22

159.4

154.0

2022-23

166.1

160.0

2023-24

173.5

167.0

Recovery Plan Projection

2024-25

179.5

173.5

2025-26

185.6

180.3

2026-27

192.2

187.3

2027-28

199.0

194.6

2028-29

206.2

202.2

2029-30

213.7

210.1

Average Annual Growth (Per Cent)

FAO Spring 2021

Average

Historical

1982-83 to 1991-92

10.1

1992-93 to 1998-99

0.5

1999-00 to 2010-11

6.6

2011-12 to 2019-20

2.6

5.4

Medium-Term

2020-21 to 2023-24

3.0

Recovery Plan

2024-25 to 2029-30

1.5

2.3

Average Annual Growth over 2024-25 to 2029-30 (Per Cent)

FAO Spring 2021

2021 Ontario Budget

Health

3.8

2.2

Education

2.3

1.2

Postsecondary Education

3.2

1.0

Children’s and Social Services

3.3

1.0

Justice

2.5

1.0

Other Expense

2.0

0.8

Total Program Expense

3.0

1.5

2021 Budget Program Spending Per Capita

(2020 Constant $)

Historical

2017-18

10632

2018-19

10678

2019-20

10521

Medium-Term Projection

2020-21

10715

2021-22

10950

2022-23

10797

2023-24

10526

2024-25

10322

2025-26

10138

Recovery Plan Projection

2026-27

9957

2027-28

9779

2028-29

9605

2029-30

9434

(Per Cent)

Long-term Average (1981-82 to 2019-20)

2020-21

2029-30

Primary Budget Balance as a share of GDP

0.4

-2.8

0.7

Overall Budget Balance as a share of GDP

-1.3

-4.2

-0.5

Net Debt as a share of GDP

26.8

46.8

44.7

Interest on Debt as a share of revenue

10.3

8.1

7.3

Footnotes

[1] See COVID-19 Vaccines for Ontario, Government of Ontario.

[2] Ibid.

[3] World Economic Outlook, International Monetary Fund, April 2021.

[4] Ibid.

[5] Federal Open Market Committee Statement, Federal Reserve, April 2021.

[6] See Explaining the Decline in Ontario Insolvencies During the Pandemic, FAO, April 2021 for an overview of how these government supports affected insolvency trends during the pandemic.

[7] Rapidly Evolving Expectations in the Housing Market, Mortgage Professionals Canada, February 2021.

[8] The policy interest rate is the Bank of Canada’s target for the overnight rate, which is the rate at which major Canadian financial institutions can borrow from one another.

[9] Bank of Canada announces the discontinuation of market functioning programs introduced during COVID-19, Bank of Canada, March 2021.

[10] Monetary Policy Report, Bank of Canada, April 2021. The Bank is generally not expected to react to monthly inflation rates that exceed the two per cent target in mid-2021 and largely reflect temporary factors.

[11] Measured by household net savings divided by household disposable income. Household net savings equals household disposable income plus change in pension entitlements minus household final consumption expenditure.

[12] Canadian Survey of Consumer Expectations: First Quarter of 2021, Bank of Canada, April 2021. Data is for Canada.

[13] Business Outlook Survey Spring 2021, Bank of Canada, April 2021. Data is for Canada.

[14] See Economic and Budget Outlook, Winter 2021 for a discussion of medium-term risks to Ontario’s economy, February 2021.

[15] Data is for May 2021. For more information on the impact of the pandemic on Ontario’s labour market, see the FAO’s report on Ontario’s Labour Market in 2020.

[16] Monetary Policy Report, Bank of Canada, April 2021.

[17] The outlook for the Ontario economy improved noticeably after the 2021 budget was prepared.

[18] Revenue from Corporations Tax (-$4.9 billion) and Sales Tax (-$2.3 billion) make up most of the overall decline in tax revenue in 2020-21.

[19] ‘Other’ revenues consist of incomes from Government Business Enterprises (GBEs) and Other Non-Tax Revenues. Income from GBEs is expected to fall by $2.0 billion in 2020-21, largely the result of a sharp drop in Ontario Lottery and Gaming Commission revenues from casino shutdowns. The reduction in Other Non-Tax Revenue was driven by a decline in Fees, Donations and Other Revenues from Hospitals, School Boards and Colleges, as well as a drop in revenue from Fees and Licences attributable to the COIVD-19 pandemic.

[20] $7.4 billion of the increase in federal transfers reflect one-time COVID-19 pandemic support. See page 160 of the 2021 Ontario Budget.

[21] The three main tax revenue categories are Personal Income Tax, Sales Tax and Corporations Tax. The discrepancy between the government economic and revenue forecast appears mainly in the Personal Income Tax and Corporations Tax revenues.

[22] The FAO's analysis of the 2019 budget found that there were unannounced tax cuts starting in 2021–22. See the FAO’s Economic and Budget Outlook, Fall 2019 for more details. The FAO’s analysis of the 2020 Ontario budget did not find any unannounced tax cuts.

[23] The earliest program spending data on a comparable basis is available from 1981–82 based on Ontario Public Accounts.

[24] From 2020–21 to 2023–24, base program spending is projected to increase by $13.3 billion, almost two-third of which is projected to be spent in 2021–22.

[25] See Page 10 in the 2021 Ontario Budget.

[26] See Ministry of Health: Spending Plan Review for details.

[27] See Ministry of Education: Spending Plan Review for details.

[28] These ministries include Transportation; Energy, Northern Development and Mines; Finance; Treasury Board Secretariat; Municipal Affairs and Housing; Government and Consumer Services; Heritage, Sport, Tourism and Culture Industries; Labour, Training and Skills Development; Agriculture, Food and Rural Affairs; Infrastructure; Economic Development, Job Creation and Trade; Environment, Conservation and Parks; Natural Resources and Forestry; Board of Internal Economy; Seniors and Accessibility; Indigenous Affairs; Executive Offices; and Francophone Affairs as well as Ontario Teachers’ Pension Plan.

[29] This will be driven by significantly higher spending in several ministries including Infrastructure, Transportation, and Energy and Northern Development Mines. Most of the increase occurs in 2021-22, after which spending for the majority of these ministries will either decline or be largely unchanged.

[30] See Table 3.12 in the 2021 Ontario Budget.

[31] For example, in the 2019 Ontario Budget, the government allocated $1.1 billion to the standard contingency funds. See Table 3.13 in the 2019 Ontario Budget for details.

[32] Despite large deficits, historically low interest rates help absorb the cost of new borrowing and debt carried over from previous years, leading to a modest increase in the interest on debt.

[33] Interest on debt is projected to increase by $1 billion from 2019-20 to 2023-24, while revenues are projected to increase by $17.4 billion over the same period.

[35] The government has presented a plan to limit spending growth by 1.5 per cent over the recovery period, well below the pace of growth in demand for program spending (see Recovery Plan expense outlook section for more details).

[36] See pages 124 and 366 of Public services for Ontarians: A Path to sustainability and excellence for a discussion of the challenges associated with achieving permanent efficiency gains. Other examples of these challenges include the province’s efforts to digitize health records (see the Ontario Auditor General’s review of eHealth).

[37] See Planned program spending growth in key sectors will be significantly slower than the demand for public services for details on the specific drivers used for each sector.

[38] See Ministry of Health: Spending Plan Review for details.

[39] See Ministry of Education: Spending Plan Review for details.

[40]See Ontario’s Fiscal Recovery Plan section for a detailed assessment of the government’s recovery plan.

[41] The increase in the general Corporations Tax rate also incorporates increases to Manufacturing and Processing Corporations Income Tax Rate and the Small Business Corporations Income Tax Rate.