Table of Abbreviations

|

Abbreviation |

Long Form |

|---|---|

|

CAD |

Canadian Dollars |

|

FAO |

Financial Accountability Office of Ontario |

|

GGRA |

Greenhouse Gas Reduction Account |

|

GHG |

Greenhouse Gas |

|

Mt |

Megatonnes (millions of tonnes) |

|

USD |

United States Dollars |

1. Essential Points

The Government of Ontario (the Province) has introduced a cap and trade program to help achieve its targets for reducing greenhouse gas emissions.

Under cap and trade, the Province would sell allowances to emit greenhouse gases. It would then spend the funds raised on initiatives to further reduce greenhouse gas emissions.

Cap and trade will likely have an impact on the Province’s surplus/deficit for several reasons:

- Whatever level of revenue the Province achieves from cap and trade, if it uses the funds to finance capital projects or programs that are already planned, cap and trade expenses would be lower than revenues, resulting in a reduction in the deficit/increase in the surplus;

- If the Province commits to spending that is difficult to reduce or stop, and revenues are lower than anticipated, the deficit could be increased or surplus reduced; and

- Finally, if the Province does not spend all of the cash raised from cap and trade in the same year, it could reduce the deficit (or increase the surplus) in that year and increase the deficit (or reduce the surplus) in future years.

2. Executive Summary

Background

The Government of Ontario (the Province) has targets for reducing greenhouse gas (GHG) emissions below their 1990 level by 2020 (15% below), 2030 (37% below) and 2050 (80% below). The cap and trade program, which will begin on January 1, 2017, is central to the Province’s plan for achieving these targets.

Under cap and trade, the Province would sell allowances to emit GHGs. The Province would record the cash raised in a Greenhouse Gas Reduction Account (GGRA) and then spend the funds on initiatives that are reasonably likely to reduce, or support the reduction of, GHGs. Under the governing legislation, the amount of cash going out cannot exceed the balance in the account. Consistent with this plan, the Province’s 2016 budget estimated that in 2017-18 cap and trade revenues would be $1.9 billion and expenses would be $1.9 billion.

Purpose of the Report

The purpose of this report is to analyze the fiscal impact of cap and trade, i.e. how cap and trade will impact the Province’s projected surplus/deficit. This report also identifies questions that if addressed would provide a better understanding of the fiscal impact of cap and trade.

Revenue Uncertainty

There are three key factors that will drive how much revenue the Province will raise from cap and trade:

- The price of allowances;

- The Canada-US dollar exchange rate, as USD auction proceeds are converted to Canadian Dollars to be recorded as revenue by the Province; and

- The number of allowances the Province will sell, as not all allowances offered for sale will necessarily be sold.

All three factors are difficult to forecast with precision. This difficulty is the result of both external factors outside of the control of the Province and to policy decisions that the Province will make in the future.

Expense Uncertainty and Fiscal Impact

Whatever amount of cash the Province raises through cap and trade, when the Province spends the cash, it will recognize associated expenses. Critically, the fiscal impact of cap and trade will come down to whether revenues will equal expenses on an annual basis. Four factors, all under the control of the Province, could cause expenses to differ from revenues, resulting in a fiscal impact.

Figure 2-1: Expense Uncertainty and Fiscal Impact

|

Factor |

Fiscal Impact |

|

|---|---|---|

|

Using cap and trade funds for previously planned spending |

||

|

If cap and trade cash were spent on previously planned programs, no new expenses would be incurred; i.e. there is new revenue, but no new expenses relative to the Province’s budgetary projections. |

Reduce deficit/increase surplus |

|

|

Using cap and trade funds to acquire capital assets |

||

|

If cap and trade cash were spent to acquire capital assets for the Province, revenues would exceed expenses because capital |

Reduce deficit/increase surplus |

|

|

Difficult-to-stop spending |

||

|

If the Province commits to expenses that are difficult to stop quickly, any unexpected shortfall in cap and trade revenue means expenses could exceed revenues. |

Increase deficit/reduce surplus |

|

|

Underspending |

||

|

If the Province does not spend all of the cash raised through cap and trade, revenues could exceed expenses in the year in which cash remains unspent. However, this cash would be available to spend in future years, potentially leading to expenses greater than revenues. |

Reduce deficit/increase surplus in one year potentially reverse in future years |

|

The information currently available suggests some cash raised through cap and trade (GGRA cash) will be used to acquire capital assets (e.g. building retrofits and Regional Express Rail), resulting in the cap and trade program generally reducing deficits/increasing surpluses. There is also the possibility that some GGRA cash will be used for programs that are already planned. To the extent this occurs, the cap and trade program will further reduce deficits/increase surpluses. In any particular year difficulties in adjusting expenses to match revenues and underspending in the GGRA could have a fiscal impact as well. Taken together, these four factors suggest cap and trade will likely impact the Province’s deficit/surplus.

Given the uncertainty surrounding revenues, and without more specific information on planned expenses, the FAO cannot forecast the fiscal impact of cap and trade in any particular year with sufficient precision to be useful. As more details emerge about cap and trade, MPPs can use these four factors as the basis for improving their understanding of the fiscal impact of the program.

Questions for the Province

Given the information currently available, these questions, if addressed, would provide a better understanding of the fiscal consequences of cap and trade.

|

Issue and Importance |

Question |

|---|---|

|

Using cap and trade funds for previously planned spending The 2016 budget shows fully offsetting revenues and expenses associated with cap and trade in the period 2015-16 to 2017-18.* This report raises questions about whether cap and trade will be fiscally neutral. A key question is whether some of funds raised through cap and trade may finance existing spending, not add to it. The greater the amount of already planned cash outlay that is financed through cap and trade, the less the incremental expenses, and the greater the impact cap and trade will have on reducing the deficit or increasing the surplus. |

Does the Province intend to spend all of the cap and trade proceeds on new initiatives? If not, how much is new expense? What is the impact on the deficit/surplus? |

|

Using cap and trade funds to acquire capital assets The Province is required to record the proceeds of allowance auctions in the GGRA. Amounts in this account can only be spent on initiatives reasonably likely to reduce, or support the reduction of, greenhouse gas emissions. The Province’s Climate Change Action Plan suggests some GGRA cash could be used to acquire capital assets. If GGRA cash were used to acquire capital assets by the Province or its consolidated entities, like Metrolinx and hospitals, the expense would be recognized over the life of the asset, not at the time of acquisition. As a result, expenses would be much lower than cash outlays. Since revenues would then be higher than expenses, the Province’s deficit would be reduced (or surplus increased). |

Does the Province plan to use the proceeds of allowance auctions to acquire capital assets by the Province and its consolidated entities? If yes, what is the impact on the deficit/surplus? |

|

Difficult-to-stop spending The latest auctions in May and August of 2016 sold only 11 and 35 per cent of the allowances offered for sale. Auction sales will always be subject to uncertainty and the results from the recent auctions highlight this fact. |

In the event that revenue earned is less than projected, will the Province continue to fund all of the programs identified in the Climate Change Action Plan? If not, how would it determine which programs would continue to receive funding and which would not? |

|

* See 2017-18 in Table 3.16 (p. 267) and Table 3.19 (p. 278) of the 2016 Ontario budget. These tables show fully offsetting revenue and expense from cap and trade in the period 2015-16 to 2017-18. |

|

3. Introduction

Background

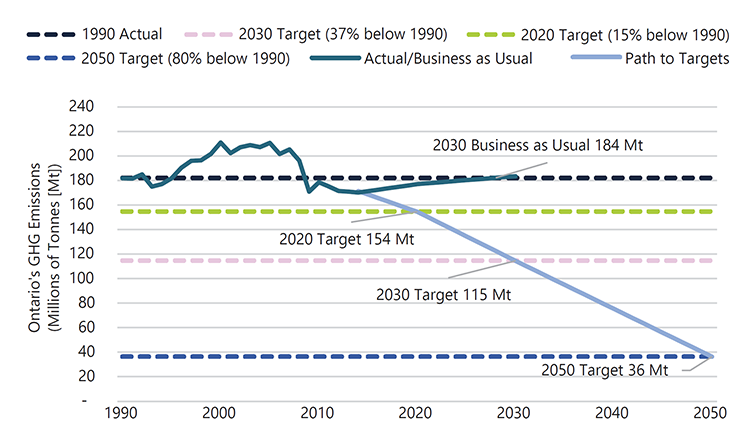

The Government of Ontario (the Province) has targets for reducing greenhouse gas (GHG) emissions below the 1990 level of 182 megatonnes (Mt) by 2020 (15% below), 2030 (37% below) and 2050 (80% below) (Figure 3‑1).

Figure 3‑1: Ontario GHG Emissions and Path to Targets

Sources: FAO analysis of Government of Canada. “National and Provincial/Territorial GHG Tables.” Web 10 May 2016. Government of Ontario. “Ontario’s Climate Change Strategy”. Web 10 May 2016; and Institute for Competitiveness and Prosperity. “Toward a low-carbon economy: The costs and benefits of cap-and-trade.” 26 April 2016: 28.

In 2015, the Province announced it would limit GHG emissions by implementing a cap and trade program. Under this program some emitters of GHGs will be required to purchase allowances created by the Province.

In order to track cash flows associated with cap and trade, the Province has established a Greenhouse Gas Reduction Account (GGRA). Under the Climate Change Mitigation and Low-carbon Economy Act, 2016[1] the Province must record in the GGRA all cash inflows from the cap and trade program. The Province must also charge to the GGRA cash outflows for administration and enforcement of the Act as well as for “initiatives ... that are reasonably likely to reduce, or support the reduction of, greenhouse gas and costs relating to any other initiatives that are reasonably likely to do so.”[2] The charges to (cash outflows from) the GGRA may not exceed the balance in the account.

The Province spent $325 million in 2015-16 through a Green Investment Fund targeted at, “fighting climate change, boosting the economy and creating jobs.”[3] Since the Province has not yet generated any revenue from cap and trade, this initial amount is described by the Province as a “down payment” on Ontario’s cap and trade program.[4] The Province’s 2016 budget projected revenue from cap and trade of $1.9 billion in 2017-18 and completely offsetting expenses of $1.9 billion.

Authority

The Financial Accountability Officer of Ontario decided to undertake the analysis presented in this report under Section 10(1)(a) of the Financial Accountability Officer Act.

Purpose

The purpose of this report is to analyze the fiscal impact of cap and trade, i.e. how cap and trade will impact the Province’s projected surplus/deficit. This report also identifies questions that if addressed would provide a better understanding of the fiscal impact of cap and trade.

Methodology

As noted above, cap and trade is designed to constrain the amount of cash spent to be no more than the amount of cash received. As such, the amount of cash coming in will determine, with some qualifications discussed below, the amount of cash going out. The design makes the fiscal analysis of cap and trade a two-part exercise. First, the FAO analyzes the factors affecting the inflow of cash, and associated revenue. Second, the FAO analyzes the outflow of cash, and associated expenses.

This report has been prepared with the benefit of information provided by the Province as well as publicly available information. Specific sources are referenced throughout.

Any dollar amounts are Canadian Dollars (CAD) except where noted. All dollar amounts are in current dollars, i.e. not adjusted for inflation.

In this report certain terms have a specific meaning that may differ from how the terms are used elsewhere.

- Cap and trade or the cap and trade program. In this report these terms mean both the allowance auction system and associated regulations and processes as well as the initiatives in the Climate Change Action Plan.

- Fiscal impact. An impact on the Province’s surplus/deficit. This report analyzes fiscal impact relative to a baseline scenario in which cap and trade, as defined above, does not exist.

Scope

This report does not:

- forecast cap and trade revenues, expenses, or cash flows;

- analyze potential economic feedback from the impacts of cap and trade on the economy to the Province’s revenues; or

- analyze any potential distributional consequences of cap and trade (e.g. re-distribution of income or wealth from one group to another in society).

4. Revenue

This chapter analyzes the factors that would affect the cash the Province would raise and the revenue that it would recognize[5] from cap and trade. The cap and trade program sells allowances at a price determined by auction (and subject to the price floor),[6] and revenue from the program will be determined by the number of allowances sold multiplied by the price per allowance.[7] There are three key factors subject to uncertainty that would affect cap and trade revenue:

- USD price of allowances set at auction;

- CAD-USD exchange rate; and

- Uncertainty associated with the number of allowances sold.

USD Price of Allowances

The final price of allowances in the seven joint auctions held by California and Quebec has been close to, or at, the floor price. The auctions set prices first in US Dollars. The past two auctions have seen demand drop, with the number of allowances offered for sale in the May and August 2016 auctions far exceeding the number sold. This drop in demand for allowances pushed settlement prices down to the price floor.

The main determinants of the USD price of allowances are:

- Program design, such as the allocation of allowances. For example, the European Union’s cap and trade program[8] issued too many allowances relative to its total emissions, leading to an oversupply of allowances and a corresponding 50 per cent drop in prices over just a few days of trading;[9],[10]

- The relative cost of switching away from carbon-intensive sources of energy.[11] If this cost falls then the price of allowances would also fall (but not below the price floor), all else being equal; and

- The level of economic activity. For example, as the economy grows more fuel tends to be consumed. This would lead to an associated increase in emissions, which would increase the demand for allowances, putting upward pressure on prices, all else being equal.[12]

Owing to a legal challenge, there is also uncertainty as to whether the Government of California will retain the authority to continue the program in its current form after 2020. Changes could impact allowance prices.

Canada-US Dollar Exchange Rate

Allowance revenue would also be affected by fluctuations in the exchange rate, since the price of allowances is determined first in US Dollars.[13],[14] The exchange rate is subject to uncertainty and recent history provides a good example of this as the Canadian Dollar went from being roughly at par with the US Dollar in January 2013, to about USD 0.70 in January 2016.[15] Figure 4‑1 provides an example of the impact the exchange rate could have on the price of allowances using the average price of USD 14.07 from the Quebec-California joint auction held in February 2016.[16]

Figure 4-1: Impact of Exchange Rates on the Price of Allowances

|

Based on the sale of 100 million allowances at USD 14.07 |

||||

|---|---|---|---|---|

|

Exchange Rate (CAD/USD) |

0.70 |

0.80 |

0.90 |

1.00 |

|

Price of Allowance (CAD) |

20.10 |

17.59 |

15.63 |

14.07 |

|

Revenue (billions CAD) |

2.0 |

1.8 |

1.6 |

1.4 |

Source: FAO

Movements in the exchange rate can have a material impact on the revenue earned. For example, in the sale of 100 million allowances at USD 14.07, each 10-cent appreciation/depreciation in the value of the CAD relative to the USD would decrease/increase revenue by about CAD 200 million.

Number of Allowances Sold

A third source of uncertainty in cap and trade revenue is the number of allowances sold. Like the other two sources of uncertainty discussed above, this variable is difficult to predict, because it depends on factors such as future economic growth, the costs of emission reduction alternatives, and expectations about future allowance prices.

The Ontario Ministry of the Environment and Climate Change anticipates it will sell all of the allowances that it offers for sale over the compliance period.[17] Eight joint auctions have been held by California and Quebec since November 2014. The latest auctions in May and August of 2016 sold only 11 and 35 per cent respectively of the offered allowances for sale.[18] Auction sales will always be subject to uncertainty and the results from the recent auctions highlight this fact.

In addition to the recent auction results, predicting the number of allowances sold is clouded by the uncertainty surrounding future policy decisions about the quantity of allowances that will be given away for free to certain emitters.

5. Expenses

Whatever amount of cash the Province raises through cap and trade, when the Province spends the cash, it will recognize associated expenses. This chapter analyzes the four factors that could cause expenses to differ from revenues, resulting in a fiscal impact:

- If cap and trade cash outlays were spent on existing programs, i.e. programs already included in the Province’s fiscal plan;

- If cap and trade cash outlays were spent to acquire capital assets for the Province;

- If the Province commits to expenses that are difficult to stop quickly and revenues were lower than expected; and

- If the Province does not spend all of the cash in the GGRA.

The sections that follow explore each factor in more detail.

Spending on Previously Planned Initiatives

The Province could use GGRA cash to pay for initiatives already included in its fiscal plan. To the extent that expenses associated with these cash outlays that are already included in the Province’s fiscal plan, the budget balance (surplus/deficit) would be improved.

Many of the initiatives listed in the Climate Change Action Plan are similar and/or related to existing initiatives. For example, the Province plans cash outlays of $160 billion between 2014-15 and 2025-26 on capital, including infrastructure, but does not indicate where all of this $160 billion will be spent beyond the two-year outlook provided in its budget.[19] It is possible that the Province may have intended to provide funds to help upgrade social housing, hospitals, universities, colleges and schools to make them more energy efficient as part of regular capital planning. Similarly, support for businesses and industries to increase their use of low-carbon technologies could displace subsidies that would have been provided through other business support programs.[20],[21]

If 10 per cent of the cash outlays from the GGRA were used for programs that were already included in the Province’s fiscal plan, the Province would recognize incremental expenses of only $0.90 for every dollar of revenue. If cap and trade were to generate revenue of $2.0 billion and 10 per cent of the associated cash outlay were already part of the fiscal plan, the Province would only recognize incremental expenses of $1.8 billion (90% of $2.0 billion). The result would be a reduction in the deficit or improvement in the surplus of $200 million.

The Province has provided only limited detail in the Climate Change Action Plan about how GGRA cash will be spent, and the Province does not disclose in detail its fiscal plan. Therefore, the FAO cannot determine the magnitude of the impact on the Province’s surplus/deficit that cap and trade might have as a result of some cash outlays paying for previously planned spending. This report simply identifies this issue as one of the areas of fiscal significance that may warrant further attention from MPPs. The following question, if addressed by the Province, would provide MPPs with a greater understanding of the fiscal impact of cap and trade.

|

Issue and Importance |

Question |

|---|---|

|

Using cap and trade funds for previously planned spending The 2016 budget shows fully offsetting revenues and expenses associated with cap and trade in the period 2015-16 to 2017-18.* This report raises questions about whether cap and trade will be fiscally neutral. A key question is whether some of funds raised through cap and trade may finance existing spending, not add to it. The greater the amount of already planned cash outlay that is financed through cap and trade, the less the incremental expenses, and the greater the impact cap and trade will have on reducing the deficit or increasing the surplus. |

Does the Province intend to spend all of the cap and trade proceeds on new initiatives? If not, how much is new expense? What is the impact on the deficit/surplus? |

|

* See 2017-18 in Table 3.16 (p. 267) and Table 3.19 (p. 278) of the 2016 Ontario budget. These tables show fully offsetting revenue and expense from cap and trade in the period 2015-16 to 2017-18. |

|

Capital Spending

FAO analysis of the Province’s Climate Change Action Plan suggests that the acquisition of capital assets may account for roughly 20 per cent of total cash outlay.[22] This estimate is subject to uncertainty, in that the FAO understands that many decisions on spending have yet to be made. Examples of likely capital acquisitions included in the Action Plan include the acceleration of the Regional Express Rail program and cash to retrofit schools, hospitals, colleges and Provincial government buildings.

Using cash from the GGRA to acquire capital assets for the Province and its consolidated entities[23] would result in cash outlays exceeding expenses. This result would occur because cash outlays for the acquisition of capital assets are recognized as expenses over the useful lives of the assets acquired, not at the time of acquisition. The implication is a reduction in the deficit or improvement in the surplus, all else being equal.

For example, if 20 per cent of the cash outlays from the GGRA were used to acquire capital assets, the Province would recognize expenses of only $0.80 for every dollar of revenue in the year of the acquisition. If cap and trade revenue were $2.0 billion and 20 per cent of the cash outlay were used to acquire capital assets, the Province might only recognize incremental expenses of $1.6 billion (80% of $2.0 billion), resulting in a reduction in the deficit or improvement in the surplus of $400 million. The reason for this is that cash outlays to acquire capital assets are recognized as expenses over the useful lives of the assets acquired. The Appendix provides further explanation.

As the Province has provided only limited detail in the Climate Change Action Plan about how GGRA cash will be spent, and the Province does not disclose details of its fiscal plan, the FAO cannot determine the magnitude of the impact of the Province’s surplus/deficit that cap and trade might have as a result of some cash outlays paying for the acquisition of capital assets. For now, this report simply identifies this issue as one of the areas of fiscal significance that may warrant further attention from MPPs. The following question, if addressed by the Province, would provide MPPs with a greater understanding of the fiscal impact of cap and trade.

|

Issue and Importance |

Question |

|---|---|

|

Using cap and trade funds to acquire capital assets The Province is required to record the proceeds of allowance auctions in the GGRA. Amounts in this account can only be spent on initiatives reasonably likely to reduce, or support the reduction of, greenhouse gas emissions. The Province’s Climate Change Action Plan suggests some GGRA cash could be used to acquire capital assets. If GGRA cash were used to acquire capital assets by the Province or its consolidated entities, like Metrolinx and hospitals, the expense would recognized over the life of the asset, not at the time of acquisition. As a result, expenses would be much lower than cash outlays. Since revenues would then be higher than expenses, the Province’s deficit would be reduced (or surplus increased). |

Does the Province plan to use the proceeds of allowance auctions to acquire capital assets by the Province and its consolidated entities? If yes, what is the impact on the deficit/surplus? |

Difficult-to-stop spending

Notwithstanding the requirement of the Climate Change Mitigation and Low-Carbon Economy Act, 2016 that charges to the GGRA may not exceed the balance in the account,[24] once the Province commits to spending, it can become difficult to reduce or cancel the spending. Given that revenues from cap and trade may fluctuate from year to year and given significant uncertainty over how much revenue will be raised, there is a risk that expenses could exceed revenues if the Province chooses initiatives that are difficult to reduce or stop.

For example, the Province had already spent $325 million in 2015-16, ahead of any revenues being recognized from cap and trade. This expense could not be stopped in the (admittedly unlikely) event that cap and trade does not raise $325 million. In that event, the Province would have to find $325 million by reducing spending, or raising revenue elsewhere, or by increasing the deficit.

Underspending

If, for whatever reason, the Province does not spend all of the cash it records in the GGRA in the same year, revenues would likely exceed expenses. This factor could lead to significant fiscal impacts from year to year. For instance, if the Province were to achieve its 2016 budget forecast cap and trade revenue of $1.9 billion in 2017-18, but owing to delays in implementing initiatives in the Climate Change Action Plan were not able to recognize expenses of $1.9 billion, the deficit would be reduced or surplus improved in that year. If the cash not spent in 2017-18 were then spent in 2018-19, cap and trade expenses would then exceed revenues, increasing the deficit or reducing the surplus, all else being equal.

6. Conclusion

This chapter summarizes the findings of this report.

Revenue Uncertainty

There are three key factors that will drive how much revenue the Province will raise from cap and trade:

- The price of emissions allowances;

- The Canada-US dollar exchange rate, as USD auction proceeds are converted to Canadian Dollars to be recorded as revenue by the Province; and

- The number of allowances the Province will sell, as not all allowances offered for sale will necessarily be sold.

All three factors are difficult to forecast with precision. This difficulty is the result of both external factors outside of the control of the Province and to policy decisions that the Province will make in the future.

Expense Uncertainty and Fiscal Impact

Whatever amount of cash the Province raises through cap and trade, when the Province spends the cash, it will recognize associated expenses. Critically, the fiscal impact of cap and trade will come down to whether revenues will equal expenses on an annual basis. Four factors, all under the control of the Province, could cause expenses to differ from revenues, resulting in a fiscal impact.

Figure 6‑1: Expense Uncertainty and Fiscal Impact

|

Factor |

Fiscal Impact |

|

|---|---|---|

|

Using cap and trade funds for previously planned spending |

||

|

If cap and trade cash were spent on previously planned programs, no new expenses would be incurred; i.e. there is new revenue, but no new expenses relative to the Province’s budgetary projections. |

Reduce deficit/increase surplus |

|

|

Using cap and trade funds to acquire capital assets |

||

|

If cap and trade cash were spent to acquire capital assets for the Province, revenues would exceed expenses because capital |

Reduce deficit/increase surplus |

|

|

Difficult-to-stop spending |

||

|

If the Province commits to expenses that are difficult to stop quickly, any unexpected shortfall in cap and trade revenue means expenses could exceed revenues. |

Increase deficit/reduce surplus |

|

|

Underspending |

||

|

If the Province does not spend all of the cash raised through cap and trade, revenues could exceed expenses in the year in which cash remains unspent. However, this cash would be available to spend in future years, potentially leading to expenses greater than revenues. |

Reduce deficit/increase surplus in one year potentially reverse in future years |

|

The information currently available suggests some cash raised through cap and trade (GGRA cash) will be used to acquire capital assets (e.g. building retrofits and Regional Express Rail), resulting in the cap and trade program generally reducing deficits/increasing surpluses. There is also the possibility that some GGRA cash will be used for programs that are already planned. To the extent this occurs, the cap and trade program will further reduce deficits/increase surpluses. In any particular year difficulties in adjusting expenses to match revenues and underspending in the GGRA could have a fiscal impact as well. Taken together, these four factors suggest cap and trade will likely impact the Province’s deficit/surplus.

Given the uncertainty surrounding revenues and without more specific information on planned expenses, the FAO cannot forecast the fiscal impact of cap and trade in any particular year with sufficient precision to be useful. As more details emerge about cap and trade, MPPs can use these four factors as the basis for improving their understanding of the fiscal impact of the program.

Questions for the Province

Given the information currently available, these questions, if addressed, would provide a better understanding of the fiscal consequences of cap and trade.

|

Issue and Importance |

Question |

|---|---|

|

Using cap and trade funds for previously planned spending The 2016 budget shows fully offsetting revenues and expenses associated with cap and trade in the period 2015-16 to 2017-18.* This report raises questions about whether cap and trade will be fiscally neutral. A key question is whether some of funds raised through cap and trade may finance existing spending, not add to it. The greater the amount of already planned cash outlay that is financed through cap and trade, the less the incremental expenses, and the greater the impact cap and trade will have on reducing the deficit or increasing the surplus. |

Does the Province intend to spend all of the cap and trade proceeds on new initiatives? If not, how much is new expense? What is the impact on the deficit/surplus? |

|

Using cap and trade funds to acquire capital assets The Province is required to record the proceeds of allowance auctions in the GGRA. Amounts in this account can only be spent on initiatives reasonably likely to reduce, or support the reduction of, greenhouse gas emissions. The Province’s Climate Change Action Plan suggests some GGRA cash could be used to acquire capital assets. If GGRA cash were used to acquire capital assets by the Province or its consolidated entities, like Metrolinx and hospitals, the expense would be recognized over the life of the asset, not at the time of acquisition. As a result, expenses would be much lower than cash outlays. Since revenues would then be higher than expenses, the Province’s deficit would be reduced (or surplus increased). |

Does the Province plan to use the proceeds of allowance auctions to acquire capital assets by the Province and its consolidated entities? If yes, what is the impact on the deficit/surplus? |

|

Difficult-to-stop spending The latest auctions in May and August of 2016 sold only 11 and 35 per cent of the allowances offered for sale. Auction sales will always be subject to uncertainty and the results from the recent auctions highlight this fact. |

In the event that revenue earned is less than projected, will the Province continue to fund all of the programs identified in the Climate Change Action Plan? If not, how would it determine which programs would continue to receive funding and which would not? |

|

* See 2017-18 in Table 3.16 (p. 267) and Table 3.19 (p. 278) of the 2016 Ontario budget. These tables show fully offsetting revenue and expense from cap and trade in the period 2015-16 to 2017-18. |

|

7. Appendix

This appendix provides a simplified and illustrative example of the mechanics of why cash outlays from the GGRA for the purposes of acquiring capital assets would lead to lower deficits/higher surpluses.

Figure 7‑1: Illustrative Example of the Fiscal Impact of Capital Acquisitions from the Greenhouse Gas Reduction Account

|

2017-18 |

2018-19 |

2019-20 |

2020-21 |

2021-22 |

2022-23 |

2023-24 |

2024-25 |

2025-26 |

2026-27 |

|

|---|---|---|---|---|---|---|---|---|---|---|

|

(1) Revenue = cash inflow |

$100 |

$100 |

$100 |

$100 |

$100 |

$100 |

$100 |

$100 |

$100 |

$100 |

|

Cash outlay |

||||||||||

|

of which for other purposes |

$80 |

$80 |

$80 |

$80 |

$80 |

$80 |

$80 |

$80 |

$80 |

$80 |

|

of which for capital acquisition |

$20 |

$20 |

$20 |

$20 |

$20 |

$20 |

$20 |

$20 |

$20 |

$20 |

|

Expenses |

||||||||||

|

Operating/transfers/other non-capital |

$80 |

$80 |

$80 |

$80 |

$80 |

$80 |

$80 |

$80 |

$80 |

$80 |

|

Amortization of capital |

- |

$0.70 |

$1.39 |

$2.09 |

$2.79 |

$3.48 |

$4.18 |

$4.87 |

$5.57 |

$6.27 |

|

(2) Total |

$80 |

$81 |

$81 |

$82 |

$83 |

$83 |

$84 |

$85 |

$86 |

$86 |

|

Surplus (Deficit) (1)-(2) |

$20 |

$19 |

$19 |

$18 |

$17 |

$17 |

$16 |

$15 |

$14 |

$14 |

This example assumes revenue of $100 in each of the next 10 years from cap and trade. This amount is recorded in the GGRA (Line 1 in Figure A-1). The FAO then assumes that all of the cash received is spent in every year, $20 to acquire capital and $80 for other purposes such as operating costs, transfer payments. The $80 for other purposes is recognized as an expense in the year in which the cash is spent. The expense associated with the $20 spent on acquiring capital is spread out over the life of the asset. The result is expenses of less than $100 over each of the next 10 years (Line 2) and a positive fiscal impact (lower deficit/higher surplus).

This example assumes an effective average asset life of 29 years, which is the Provincial average for 2011-12 to 2014-15. For example, the $20 spent in the first year, 2017-18 is recognized in equal parts over the next 29 years, about $0.70 per year. $0.70 is the amortization expense in the second year, 2018-19. Each year an additional $20 is spent acquiring capital assets, and so the amortization expense grows as more assets are acquired.

8. About this Document

Established by the Financial Accountability Officer Act, 2013, the Financial Accountability Office (FAO) provides independent analysis on the state of the Province’s finances, trends in the provincial economy and related matters important to the Legislative Assembly of Ontario.

The FAO produces independent analysis on the initiative of the Financial Accountability Officer. Upon request from a member or committee of the Assembly, the officer may also direct the FAO to undertake research to estimate the financial costs or financial benefits to the Province of any bill or proposal under the jurisdiction of the legislature.

This report was prepared on the initiative of the Financial Accountability Officer. In keeping with the FAO’s mandate to provide the Legislative Assembly of Ontario with independent economic and financial analysis, this report makes no recommendations.

The analysis was prepared by Greg Hunter under the direction of Peter Harrison. A number of external reviewers reviewed the report. The assistance of external reviewers implies no responsibility for the final product, which rests solely with the FAO.

[1] Section 71.

[2] Section 71.

[3] Government of Ontario. “Green Investment Fund.” Updated 17 March 2016. Web 16 May 2016.

[4] Government of Ontario. “Ontario Posts Final Cap and Trade Regulation.” Web 19 May 2016.

[5] Based on discussions with the Province, the FAO expects that revenue associated with the sale of allowances will be recognized in the year to which it pertains (i.e. its vintage). The Province indicates that it has yet to conclude its assessment of options for the accounting treatment of some aspects of the program (e.g., vintages). The approach to vintages will be determined in advance of the requirement to record the proceeds from the first auction (Ontario only) in March 2017. (Correspondence with the Ministry of the Environment and Climate Change: 22 August 2016.) For example, when allowances are auctioned in 2017, the majority will be of the 2017 vintage and a smaller amount will be of vintage 2020. The revenue earned from the sale of 2017 vintage allowances will be recognized as revenue in 2017 and revenue earned from the sale of 2020 vintage allowances will be deferred to 2020 and recognized as revenue in that year. The FAO has not considered further the deferral of revenue.

[6] The cap and trade program sets an auction floor price, which is the minimum price at which allowances will be sold.

[7] In reality the Province may also recognize some revenues associated with administrative penalties and other fees. The FAO expects such amount to be small in relation to revenue from the auction of allowances and has not explicitly analyzed these revenues.

[8] Called the Emissions Trading System.

[9] Chevallier, Julien. "Carbon price drivers: an updated literature review." Available at SSRN 1811963. 2011:2.

[10] The price would not fall below the floor but fewer allowances could be sold.

[11] Chevallier, Julien. "Carbon price drivers: an updated literature review." Available at SSRN 1811963. 2011:2.

[12] Chevallier, Julien. "A model of carbon price interactions with macroeconomic and energy dynamics." Energy Economics 33.6 (2011): 1295-1312.

[13] Government of Quebec. “2016 Auction Examples.” 18 Dec. 2015. Web 2 May 2016: 1.

[14] Participants have the choice to submit bids in USD or CAD at a predetermined exchange rate.

[15] Bank of Canada. “Monthly Average Exchange Rates: 10-Year Lookup.” Web 15 April 2016.

[16] California Air Resources Board and Government of Quebec. “CA-QC Joint Auction Summary Results Report.” State of California and Government of Quebec. 25 May 2016.

[17] FAO meeting with the Ministry of the Environment and Climate Change. May 10, 2016.

[18] California Air Resources Board. “California Cap-and-Trade Program Summary of Auction Settlement Prices and Results.” State of California. Update August 2016. Web 13 Sept 2016.

[19] Ontario Ministry of Finance. “2016 Ontario Budget: Jobs for Today and Tomorrow.” Queen’s Printer for Ontario, 2016: 317.

[20] Government of Ontario. “Climate Change Action Plan.” 8 June 2016.

[21] These examples are for illustrative purposes only; full examination of the Climate Change Action Plan is beyond the scope of this report.

[22] Government of Ontario. “Climate Change Action Plan.” 8 June 2016.

[23] Transfers of cash for the acquisition of capital assets at non-consolidated entities such as universities would be expensed at the time of the transfer, and so would not cause a difference in the timing of cash outlays and the associated expenses. A list of consolidated entities can be found in Schedule 8 of the Province’s 2014-15 financial statements (See page 92 of Government of Ontario (2015) “Annual Report and Consolidated Financial Statements.”).

[24] Section 71.

[25] The Province notes that measures are in place to reduce or stop spending if proceeds from cap and trade are less than anticipated. Under the GGRA spending cannot exceed the amount of proceeds taken in from the cap and trade program. All proposed spending will be reviewed and evaluated by the Minister of the Environment and Climate Change and approved by Treasury Board, and there are appropriate reporting requirements, control measures and governance structures in place.

Figure 3-1 This chart shows the Government of Ontario’s targets for reducing greenhouse gas emissions below the 1990 level of 182 megatonnes. The target for 2020 is 154 megatonnes or 15 per cent below 1990; the target for 2030 is 115 megatonnes or 37 per cent below 1990; and the target for 2050 is 36 megatonnes or 80 per cent below 1990.